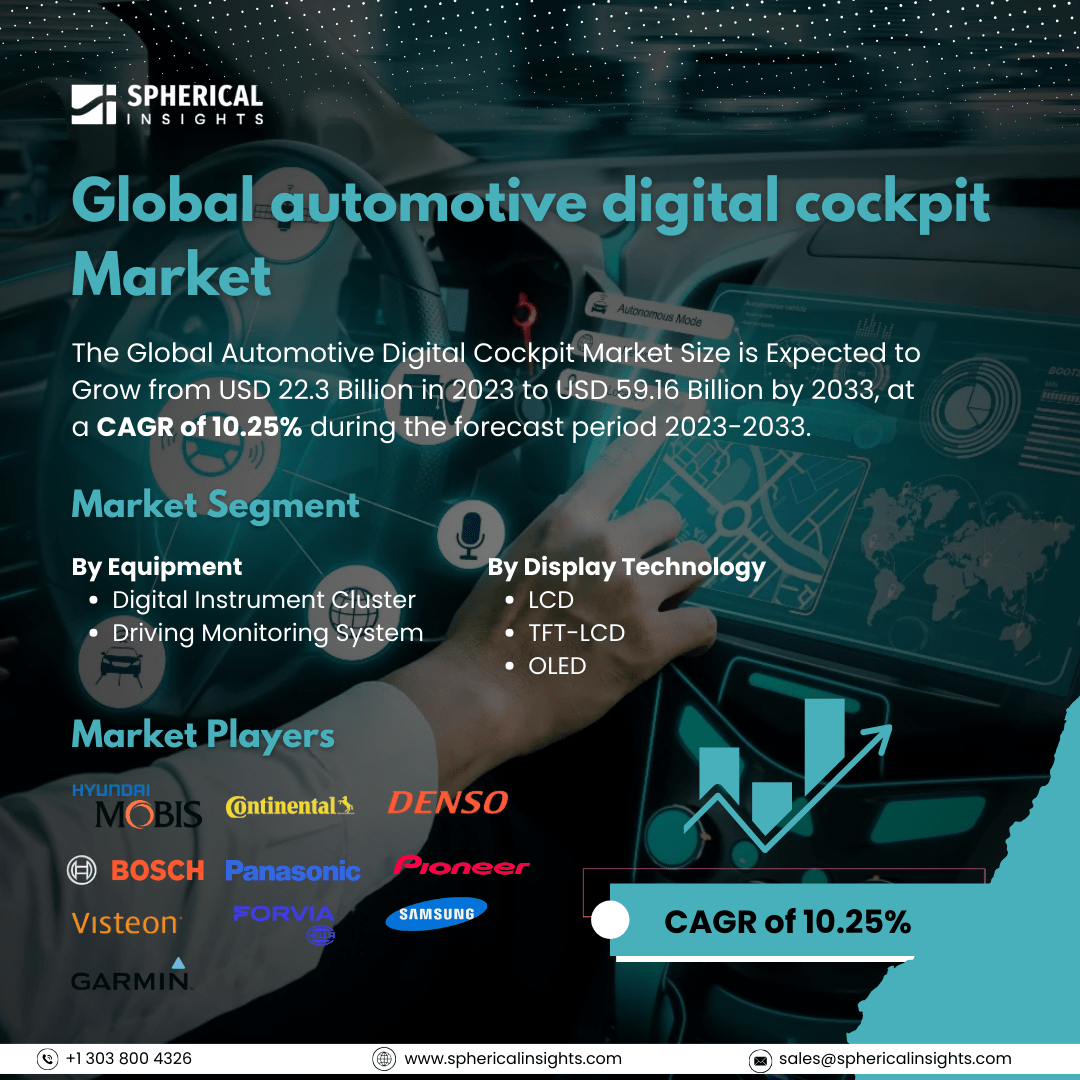

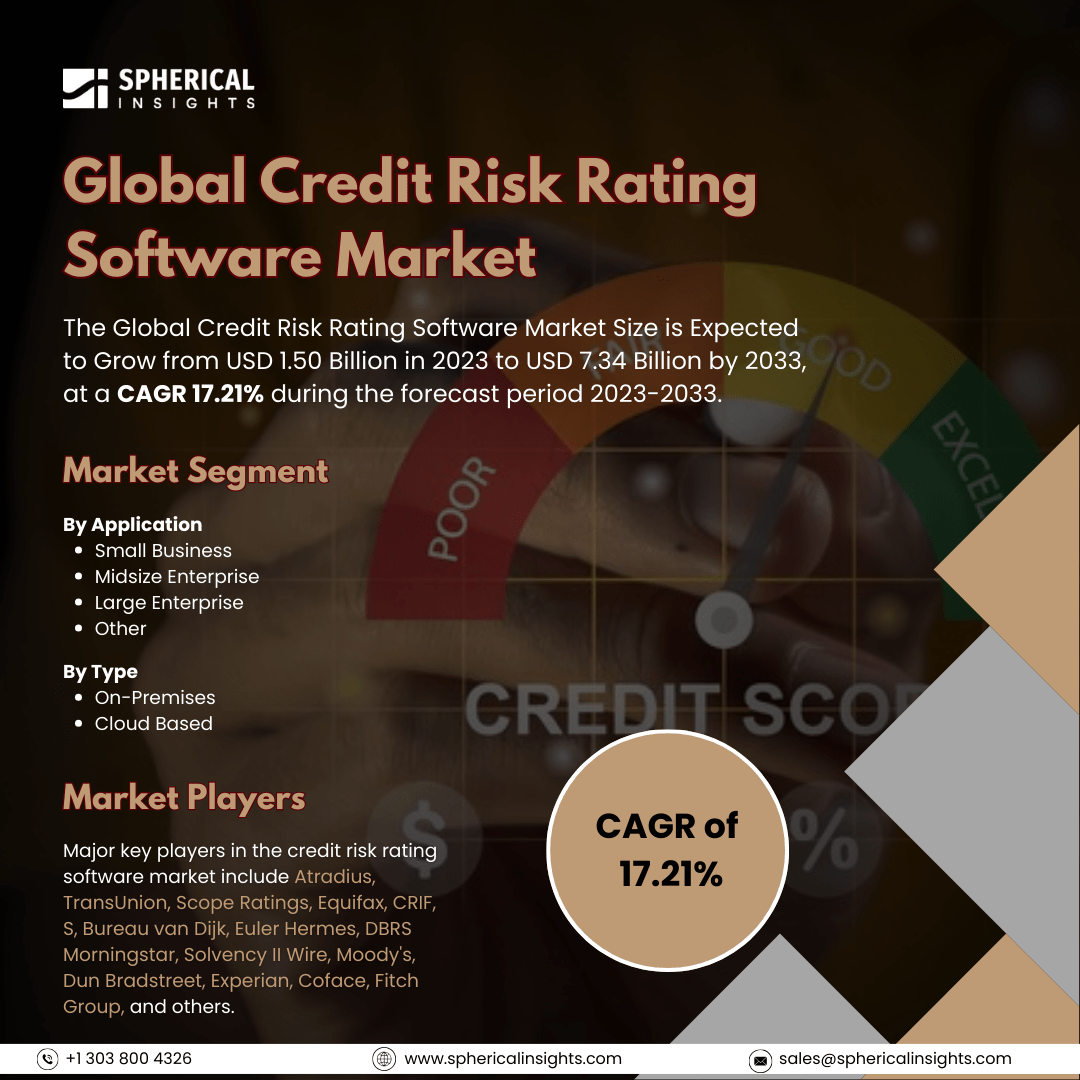

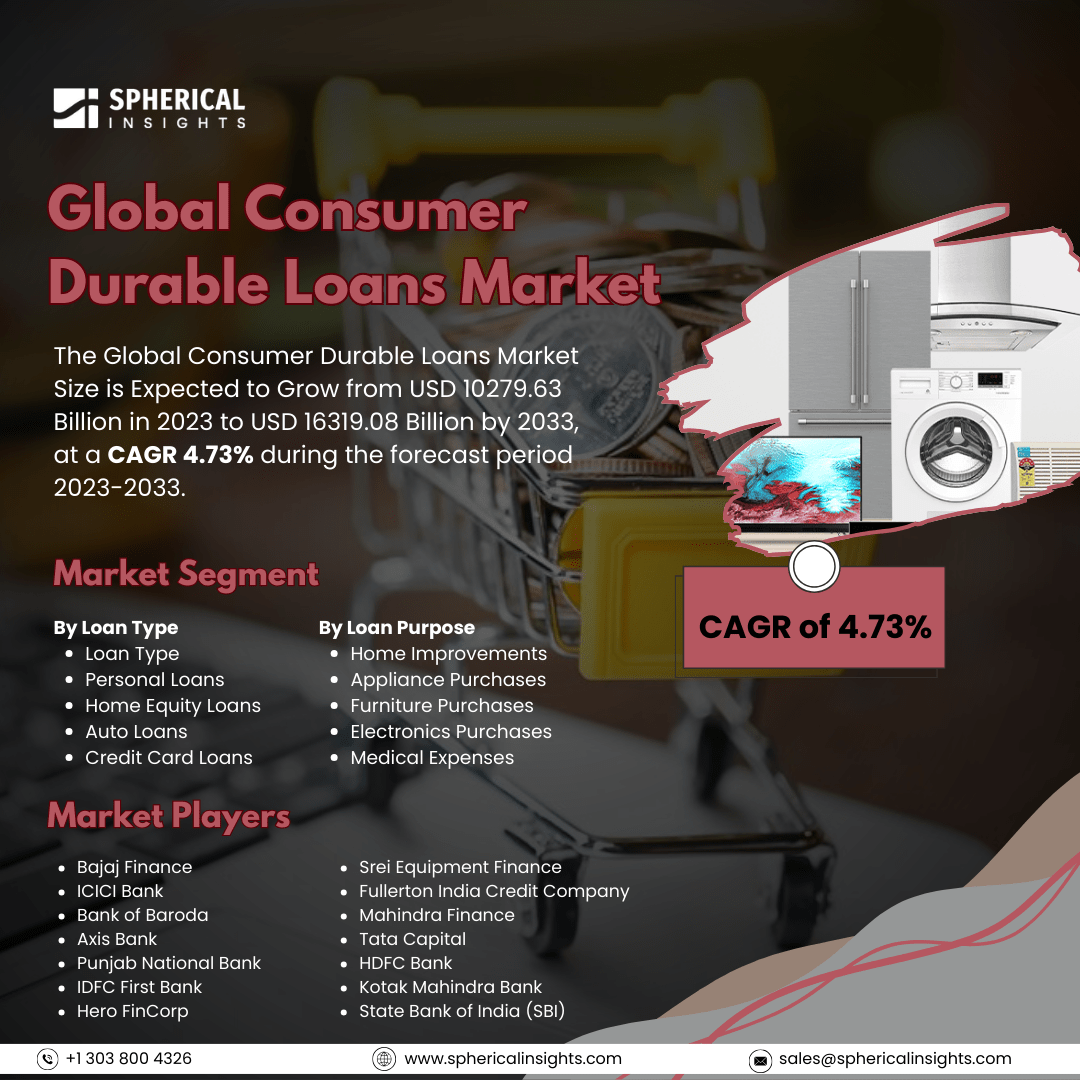

Global automotive digital cockpit Market Size to worth USD 59.16 Billion by 2033

According to a research report published by Spherical Insights & Consulting, The Global Automotive Digital Cockpit Market Size is Expected to Grow from USD 22.3 Billion in 2023 to USD 59.16 Billion by 2033, at a CAGR of 10.25 % during the forecast period 2023-2033.

Browse key industry insights spread across 210 pages with 110 Market data tables and figures & charts from the report on the Global Automotive Digital Cockpit Market Size, Share, and COVID-19 Impact Analysis, By Equipment (Digital Instrument Cluster and Driving Monitoring System), By Display Technology (LCD, TFT-LCD, and OLED), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 – 2033.

The automotive digital cockpit market encompasses advanced in-vehicle digital interfaces that integrate infotainment systems, instrument clusters, head-up displays, and connectivity solutions to enhance the driving experience. These systems incorporate cutting-edge technologies such as artificial intelligence, augmented reality, and voice recognition, providing real-time vehicle diagnostics, navigation, and entertainment features. The market is experiencing substantial growth due to the increasing demand for enhanced user experience, connectivity, and automation in modern vehicles. Several factors are driving the expansion of the automotive digital cockpit market. The rising adoption of electric vehicles (EVs) and autonomous driving technologies has significantly accelerated the integration of digital cockpits, as these vehicles require advanced human-machine interfaces. Additionally, consumer demand for personalized and connected vehicle experiences, coupled with regulatory initiatives promoting vehicle safety through advanced driver-assistance systems (ADAS), is further propelling market growth. The rapid advancements in display technology, including OLED and curved displays, have also contributed to the widespread adoption of digital cockpits. However, market growth is restrained by the high development and integration costs associated with digital cockpit systems.

The driving monitoring systems segment accounted for the highest share in 2023 and is expected to grow at a significant CAGR during the forecast period.

Based on the equipment, the automotive digital cockpit market is divided into digital instrument clusters and driving monitoring systems. Among these, the driving monitoring systems segment accounted for the largest share in 2023 and is expected to grow at a significant CAGR during the forecast period. This segment is expected to continue its significant growth during the forecast period, driven by increasing safety regulations and the rising adoption of advanced driver assistance systems (ADAS).

The LCD segment accounted for the largest share in 2023 and is expected to grow at a significant CAGR during the forecast period.

Based on the display technology, the automotive digital cockpit market is classified into LCD, TFT-LCD, and OLED. Among these, the LCD segment accounted for the largest share in 2023 and is expected to grow at a significant CAGR during the forecast period. This dominance is attributed to LCDs' cost-effectiveness and widespread adoption of in-vehicle displays.

Asia-Pacific is estimated to hold the greatest automotive digital cockpit market share over the forecast period.

Asia-Pacific is estimated to hold the greatest automotive digital cockpit market share over the forecast period. The region's continued rapid pace of vehicle sales as well as the need for advanced vehicular technologies to enhance passenger experience has forced companies to launch innovative solutions in the industry. Additionally, the increasing popularity of electric vehicles, especially in economies such as India and China, has driven recent market growth. With consumers demanding connection, personalization, and simplicity of integration from their smartphones into their vehicles, manufacturers are feeling pressure to increase their digital cockpit production.

Latin America is predicted to have the fastest CAGR growth in the automotive digital cockpit market over the forecast period. Brazil and Mexico are witnessing high-scale development activities that have seen large sales of passenger and commercial vehicles. Consumers in this region are quickly adopting connected vehicles because advanced technologies are becoming increasingly accessible and the presence of major digital cockpit solution providers is on the rise.

Company Profiling

Major key players in the automotive digital cockpit market are HYUNDAI MOBIS, Robert Bosch GmbH, Visteon Corporation, Continental AG, DENSO CORPORATION, Panasonic Holdings Corporation, Pioneer Corporation, SAMSUNG, FORVIA, Garmin Ltd., and others.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In October 2024, HYUNDAI MOBIS announced a Business Cooperation Agreement with the German optoelectronics company ZEISS. Under this agreement, the companies would collaborate in developing the 'Holographic Windshield Display' at the former's technical research center located in Yongin, Gyeonggi-do. The Holographic HUD technology uses the windshield as a transparent display to display a variety of driving information and can also make use of infotainment functions like videos, music, and games at the same time. The companies are targeting the year 2027 to start mass production of this technology.

Market Segment

This study forecasts global, regional, and country revenue from 2023 to 2033. Spherical Insights has segmented the automotive digital cockpit market based on the below-mentioned segments:

Global Automotive Digital Cockpit Market, By Equipment

- Digital Instrument Cluster

- Driving Monitoring System

Global Automotive Digital Cockpit Market, By Display Technology

Global Automotive Digital Cockpit Market, By Regional Analysis

- North America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa