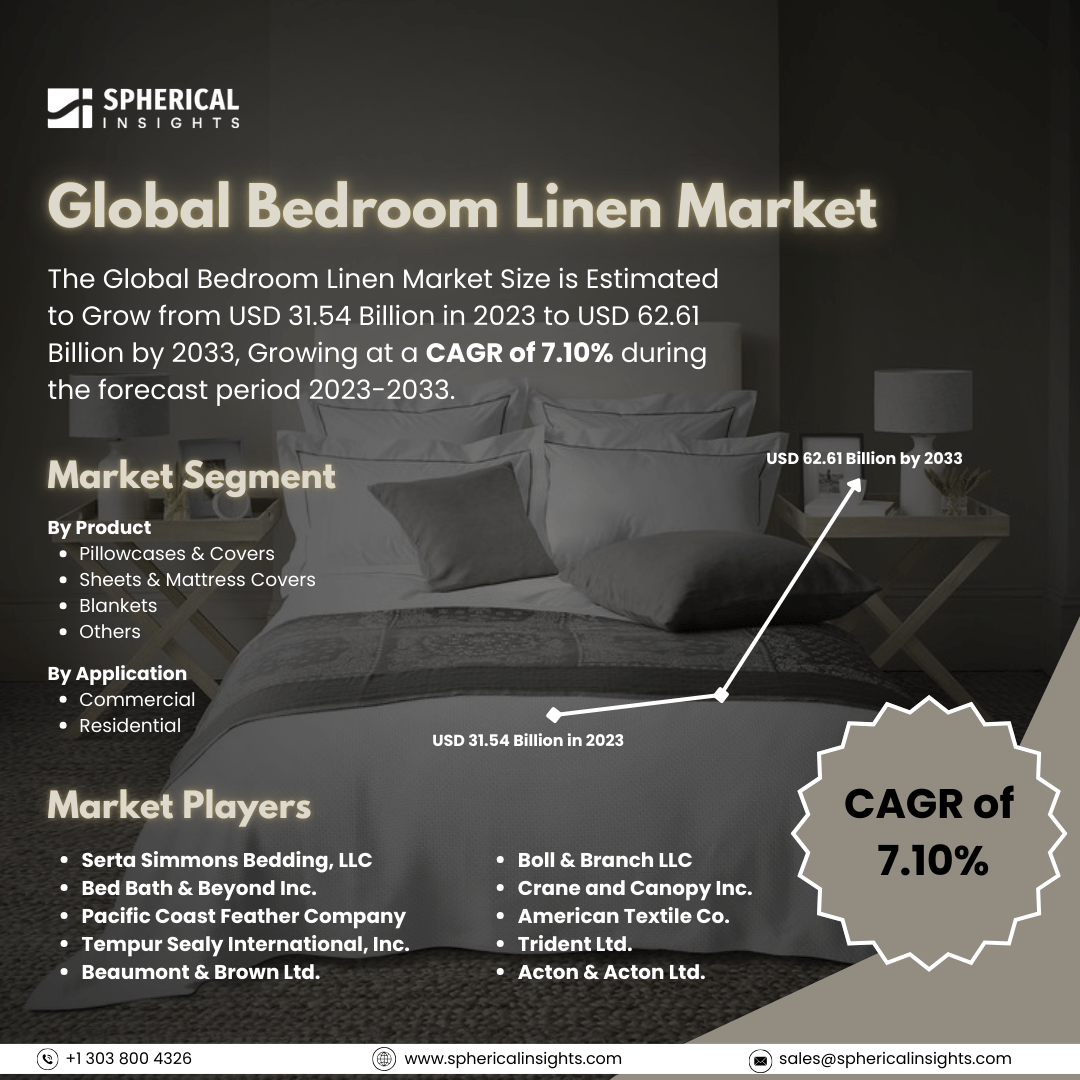

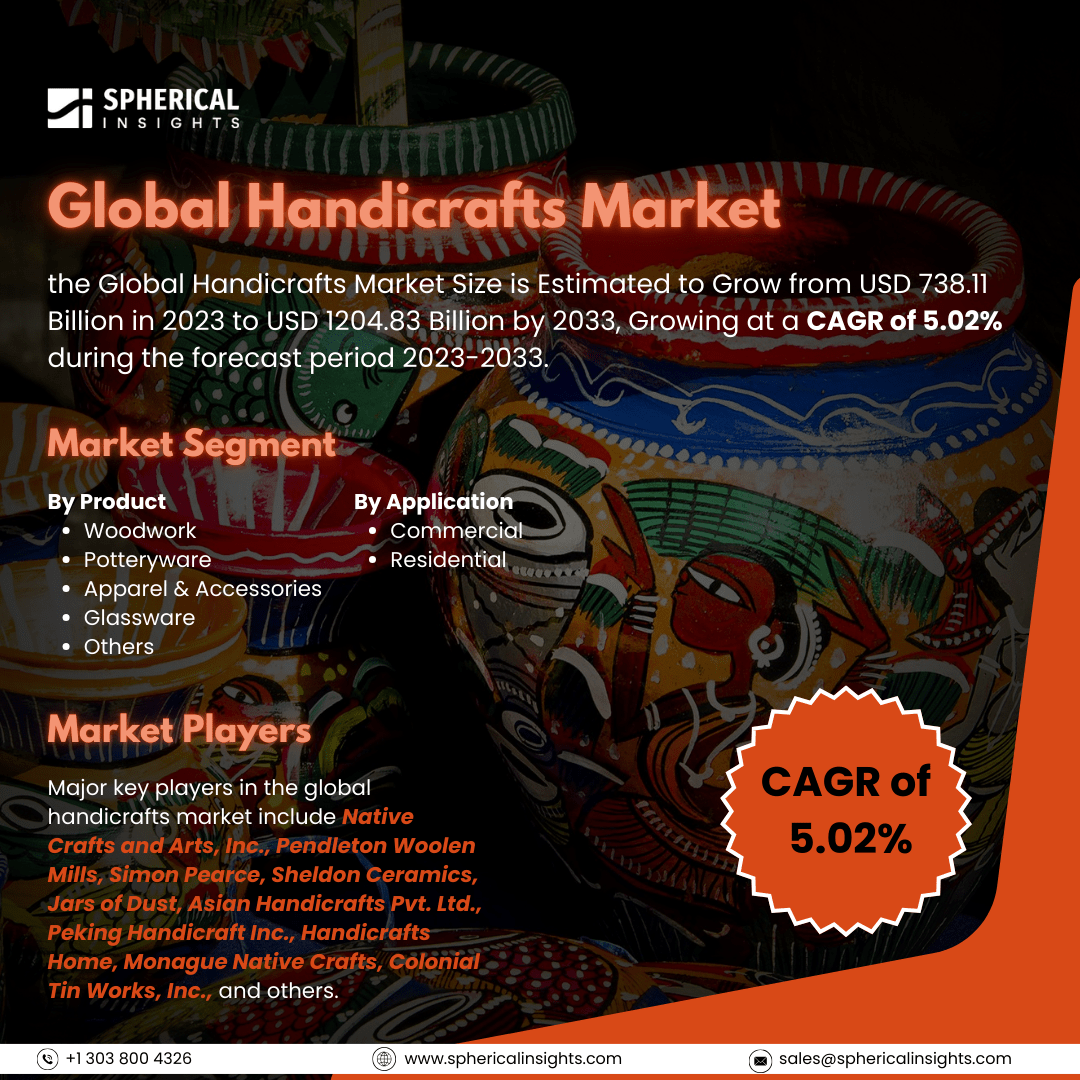

Global Green Steel Market Size to worth USD 1224.32 Billion by 2033

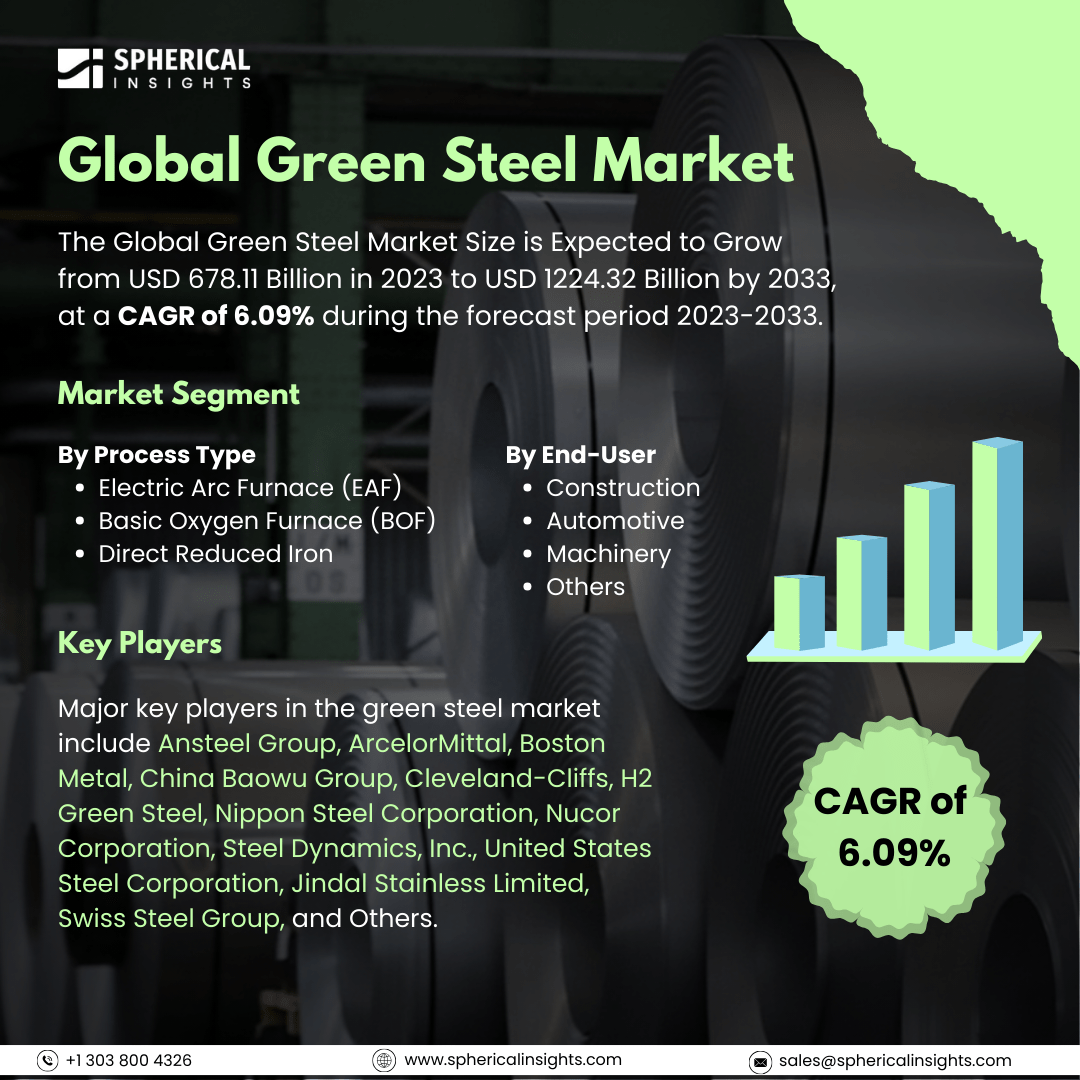

According to a research report published by Spherical Insights & Consulting, The Global Green Steel Market Size is Expected to Grow from USD 678.11 Billion in 2023 to USD 1224.32 Billion by 2033, at a CAGR of 6.09% during the forecast period 2023-2033.

Browse key industry insights spread across 210 pages with 110 Market data tables and figures & charts from the report on the Global Green Steel Market Size, Share, and COVID-19 Impact Analysis, By Process Type (Electric Arc Furnace (EAF), Basic Oxygen Furnace (BOF), and Direct Reduced Iron), By End-User (Construction, Automotive, Machinery, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 – 2033.

Steel manufacturing and delivery using low-carbon or zero-carbon methods is referred to as the green steel market. Since conventional steel production techniques mostly rely on coal and other fossil fuels, green steel seeks to drastically cut or completely eradicate greenhouse gas emissions. With a far smaller carbon footprint, this industry involves the development and application of alternative energy sources like hydrogen and renewable electricity to power steelmaking operations. Green steel production is expected to grow significantly in the next decade due to global environmental regulations and carbon emission reduction efforts. Major steel companies are investing in low-carbon technologies and governments are supporting green steel development through policy pushes and public funding. Various government initiatives drive the market of green steel. For instance, the Indian government launched the Green Steel Mission, funded by RS 15,000 crore, to aid the steel sector in reducing carbon emissions and achieving the Net Zero Target, through a Production-Linked Incentive Scheme, renewable energy incentives, and government agency procurement requirements. However, the global green steel market faces challenges due to capital investments, upfront costs, and the need for significant infrastructure upgrades and carbon capture technologies.

The electric arc furnace (EAF) segment accounted for the highest share of 41.1% in 2023 and is expected to grow at a significant CAGR during the forecast period.

Based on the process type, the green steel market is classified into electric arc furnace (EAF), basic oxygen furnace (BOF), and direct reduced iron. Among these, the electric arc furnace (EAF) segment accounted for the highest share of 41.1% in 2023 and is expected to grow at a significant CAGR during the forecast period. EAF's effectiveness and adaptability make it easier to recycle waste metal into new steel products. As closed-loop manufacturing and sustainability gain popularity, steelmakers looking to reduce their environmental effects find EAF to be quite appealing.

The automotive segment accounted for the highest share of 37.2% in 2023 and is expected to grow at a significant CAGR during the forecast period.

Based on the end-user, the green steel market is divided into construction, automotive, machinery, and others. Among these, the automotive segment accounted for the highest share of 37.2% in 2023 and is expected to grow at a significant CAGR during the forecast period. This is because of the ongoing need for steel grades that are both strong and lightweight. Automakers must use advanced high-strength steels (AHSS) and other innovative alloying procedures to reduce mass to comply with stricter car emission rules.

Europe is estimated to hold the largest share of the green steel market over the forecast period.

Europe is estimated to hold the largest share of the green steel market over the forecast period. The bloc's steel manufacturing sector is strong in large nations including France, Spain, Italy, and Germany. In addition, the European Commission has led the charge in encouraging sustainable practices and has put strong rules in place to lower carbon emissions from heavy industries like steel manufacturing.

Asia Pacific is predicted to have the fastest CAGR growth in the green steel market over the forecast period. China, India, Indonesia, and Vietnam, with their vast raw material reserves and rapidly growing manufacturing sector, are experiencing high pollution levels due to traditional coal-based steel production methods, prompting governments to promote low-carbon alternatives and green steel imports to meet environmental regulations.

Company Profiling

Major key players in the green steel market include Ansteel Group, ArcelorMittal, Boston Metal, China Baowu Group, Cleveland-Cliffs, H2 Green Steel, Nippon Steel Corporation, Nucor Corporation, Steel Dynamics, Inc., United States Steel Corporation, Jindal Stainless Limited, Swiss Steel Group, and Others.

Recent Development

- In December 2024, India was the first nation to establish and implement the Green Steel Taxonomy. This framework establishes precise guidelines for assessing and approving steel products according to their effects on the environment. The taxonomy encourages cleaner production methods by classifying steel into various star grades according to its carbon emissions.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at global, regional, and country levels from 2023 to 2033. Spherical Insights has segmented the green steel market based on the below-mentioned segments:

Global Green Steel Market, By Process Type

- Electric Arc Furnace (EAF)

- Basic Oxygen Furnace (BOF)

- Direct Reduced Iron

Global Green Steel Market, By End-User

- Construction

- Automotive

- Machinery

- Others

Global Green Steel Market, By Regional Analysis

- North America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa