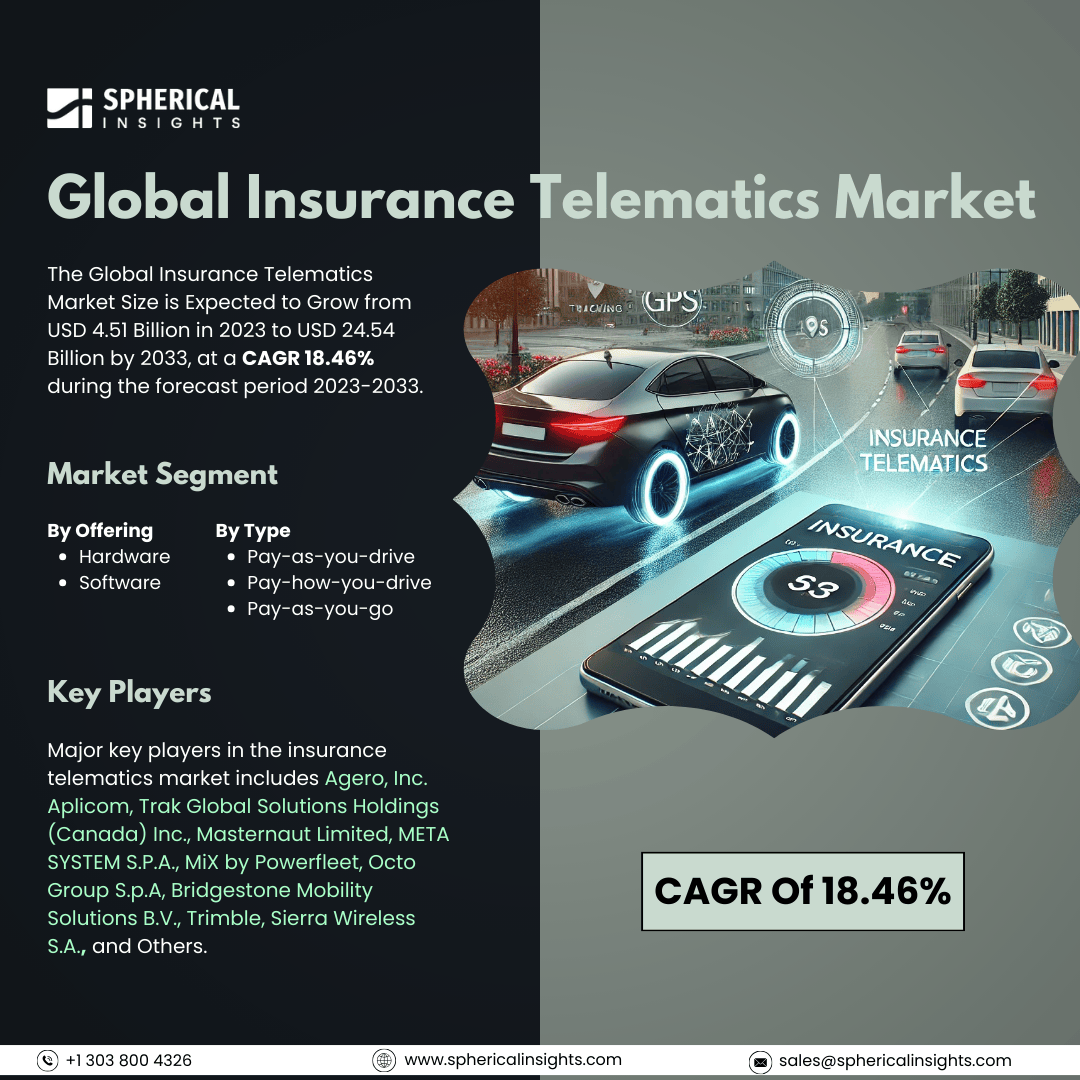

Global Insurance Telematics Market Size to worth USD 24.54 Billion by 2033

According to a research report published by Spherical Insights & Consulting, The Global Insurance Telematics Market Size is Expected to Grow from USD 4.51 Billion in 2023 to USD 24.54 Billion by 2033, at a CAGR 18.46% during the forecast period 2023-2033.

Browse key industry insights spread across 210 pages with 110 Market data tables and figures & charts from the report on the Global Insurance Telematics Market Size, Share, and COVID-19 Impact Analysis, By Type (Hardware, Software), By Offering (Pay-As-You-Drive, Pay-How-You-Drive, and Pay-As-You-Go), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 – 2033.

The insurance telematics market involves the use of technology to monitor and assess driving behavior, which helps create personalized insurance policies. A telematics device or application is installed in the vehicle to collect data on driving habits such as speed, distance, braking, and location. This information is utilized to assess risk and determine insurance premiums. Several factors are driving the growth of the insurance telematics market. Consumers are becoming increasingly aware of their driving habits and prefer insurance products that reflect their behavior. Telematics enables insurers to offer usage-based insurance (UBI), which can provide lower premiums for low-risk drivers. By identifying risky driving behaviors like speeding, hard braking, and sharp cornering, telematics data helps insurers promote safer driving habits and reduce claims. However, there are several primary challenges that could restrain the growth of the insurance telematics market. These include consumer privacy concerns regarding the collection and use of driving data, including location tracking and driving habits which can feel intrusive. There are also worries about potential data security breaches and a lack of transparency from insurers about how this data is used. Additional challenges include difficulties with device installation, potential issues with data portability when switching insurers, and regulatory complexities across different regions, all of which can hinder market expansion.

The software segment is predicted to hold the largest market share through the forecast period.

Based on the type, the insurance telematics market is classified into hardware, software. Among these, the software segment is predicted to hold the largest market share through the forecast period. The growing demand for advanced analytics and data processing capabilities as organizations recognize the importance of leveraging real-time data to enhance decision-making, improve customer experiences, and streamline operations. As such, software solutions that facilitate effective telematics integration are becoming essential. The rise of cloud-based technologies and the increasing adoption of Internet of Things (IoT) devices are further driving the expansion of the software segment, enabling seamless data communication and analysis.

The pay-as-you-drive segment is anticipated to hold the highest market share during the projected timeframe.

Based on the offering, the insurance telematics market is divided into pay-as-you-drive, pay-how-you-drive, and pay-as-you-go. Among these, the pay-as-you-drive segment is anticipated to hold the highest market share during the projected timeframe. This growth is largely due to the increasing preference for usage-based insurance models among consumers. This shift is driven by a rising awareness of cost savings and the availability of personalized insurance premiums that reflect actual driving behaviour. As more insurers and technology providers develop solutions to monitor driving habits in real-time, the appeal of pay-as-you-drive policies is growing, encouraging greater adoption among both consumers and insurers. This trend is also supported by advancements in telematics technology, making it easier to track and analyze driving patterns.

North America is estimated to hold the largest share of the insurance telematics market over the forecast period.

North America is estimated to hold the largest share of the insurance telematics market over the forecast period. This is primarily due to the early adoption of advanced telematics solutions and a strong regulatory framework. The region's well-established automotive industry and the presence of key players in the technology and insurance sectors contribute to a robust ecosystem for telematics applications. Additionally, the increasing focus on customer-centric insurance models and the demand for enhanced driver safety and risk management solutions are driving market growth. As consumers seek innovative insurance products that leverage data-driven insights, North America remains a significant hub for insurance telematics.

Europe is expected to grow the fastest during the forecast period. The growth is driven by a combination of regulatory support and consumer awareness concerning telematics-based insurance solutions. The European Union’s emphasis on sustainability and road safety initiatives is motivating insurers to adopt innovative telematics technologies that promote responsible driving. Furthermore, the rise of smart mobility solutions and the increasing integration of telematics in vehicles are enhancing the attractiveness of usage-based insurance models. As consumers become more receptive to personalized insurance options, Europe is positioned to lead in the adoption of advanced telematics solutions.

Company Profiling

Major key players in the insurance telematics market includes Agero, Inc. Aplicom, Trak Global Solutions Holdings (Canada) Inc., Masternaut Limited, META SYSTEM S.P.A., MiX by Powerfleet, Octo Group S.p.A, Bridgestone Mobility Solutions B.V., Trimble, Sierra Wireless S.A., and Others.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In August 2024, Zuno General Insurance has introduced a new coverage option for customers with the Private Car Package and the Private Car Stand Alone Own Damage Policy (SAOD). This option, called "Pay How You Drive," allows users to evaluate their driving skills and receive an objective score known as the Zuno Driving Quotient. Additionally, users can earn rewards for safe driving.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2023 to 2033. Spherical Insights has segmented the insurance telematics market based on the below-mentioned segments:

Global Insurance Telematics Market, By Offering

Global Insurance Telematics Market, By Type

- Pay-as-you-drive

- Pay-how-you-drive

- Pay-as-you-go

Global Insurance Telematics Market, By Regional Analysis

- North America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa