Global Aircraft Carrier Market Size To Worth USD 2.6 Billion By 2033 | CAGR Of 6.39%

Category: Aerospace & DefenseGlobal Aircraft Carrier Market Size To Worth USD 2.6 Billion By 2033

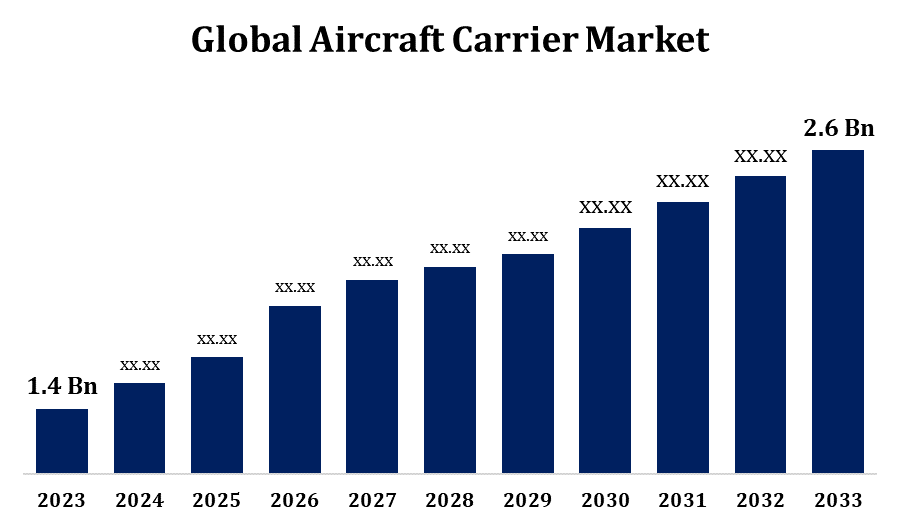

According to a research report published by Spherical Insights & Consulting, the Global Aircraft Carrier Market Size to Grow from USD 1.4 Billion in 2023 to USD 2.6 Billion by 2033, at a Compound Annual Growth Rate (CAGR) of 6.39% during the forecast period.

Get more details on this report -

Browse key industry insights spread across 211 pages with 120 Market data tables and figures & charts from the report on the "Global Aircraft Carrier Market Size, Share, and COVID-19 Impact Analysis, by Type (Conventional-Powered and Nuclear-Powered), Configuration (Catapult-Assisted Take-Off but Arrested Recovery, Short Take-Off but Arrested Recovery, and Short Take-Off but Vertical Recovery), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033." Get Detailed Report Description Here: https://www.sphericalinsights.com/reports/aircraft-carrier-market

The aircraft carrier market is expanding rapidly, spurred by growing defence budgets and geopolitical concerns. Major players such as the United States, China, and India are investing considerably in the construction and modernisation of their naval forces. Advances in nuclear propulsion, stealth technology, and automation are driving industry growth, improving operating efficiency and combat capabilities. Integration of unmanned systems with advanced sensing technologies is an emerging topic. North America leads the market, followed by Asia-Pacific, owing to significant military spending and technical breakthroughs. High expenses, extended development schedules, and a shortage of experienced workers are among the challenges. Despite this, the market forecast remains optimistic, driven by ongoing innovation and critical military imperatives.

Aircraft Carrier Market Value Chain Analysis

The aircraft carrier market value chain includes several essential stages, ranging from original design to deployment and maintenance. It starts with research and development (R&D), which involves collaborations among defence agencies, naval architects, and technology vendors to create and design next-generation carriers. Following that, component manufacturing include creating high-quality materials, propulsion systems, and avionics. Major shipbuilders supervise the assembly process, which combines various components to create a coherent vessel. After construction, the commissioning phase comprises rigorous testing and personnel training. MRO services ensure that the carrier remains operational during its lifespan. Key players include government defence departments, contractors, subcontractors, and suppliers. Technological improvements and regulatory frameworks further support the value chain, ensuring increased capabilities and strategic military superiority.

Aircraft Carrier Market Opportunity Analysis

Rising defence spending and geopolitical concerns are driving the aircraft carrier market, creating substantial prospects. The development of improved nuclear-powered carriers with increased operational range and efficiency is a key growth area. Innovations in stealth technology and unmanned aerial system integration open up new possibilities, allowing for increased tactical agility and reduced crew requirements. Emerging markets, notably in Asia-Pacific, are boosting their investment in naval capabilities, creating opportunities for new contracts and cooperation. Furthermore, the need to modernise ageing fleets in established areas such as North America and Europe demonstrates the need for cutting-edge retrofits and upgrades.

The government's focus on improving naval capabilities is largely fuelling growth in the aircraft carrier market. Increased defence resources and strategic objectives highlight the need of modernising and expanding naval forces. This change is intended to resolve geopolitical issues, protect marine interests, and strengthen power projection capabilities. To ensure naval superiority, investments on next-generation carriers equipped with modern technology such as nuclear propulsion and stealth features are prioritised. Furthermore, government-funded R&D initiatives and collaborations with defence contractors promote innovation and shorten development times. The emphasis on fleet modernisation, which includes retrofits and technological upgrades, drives increasing market demand.

High expenses involved with research, development, and construction create enormous financial barriers, necessitating large government financing and long-term commitments. Extended development and construction durations can cause delays and increased costs. Technological complexity needs skilled labour and advanced expertise, both of which are sometimes in limited supply. Furthermore, maintaining and updating existing fleets is resource-intensive, requiring ongoing MRO efforts. Geopolitical uncertainties and shifting defence objectives can have an impact on budget allocations and procurement plans.

Insights by Type

The nuclear power type segment accounted for the largest market share over the forecast period 2023 to 2033. Nuclear-powered carriers provide major advantages, such as extended operational range without the need for frequent refuelling, increased endurance, and faster speeds, all of which are vital for long-term military operations and rapid deployment. Key players, primarily the United States and, increasingly, China, are prioritising the development and deployment of nuclear-powered carriers to improve strategic capabilities. Technological developments in reactor design and safety features contribute to the segment's growth.

Insights by Confuguration

The Catapult-Assisted Take-Off but Arrested Recovery segment accounted for the largest market share over the forecast period 2023 to 2033. This technique, predominantly used by sophisticated navies such as the United States and France, allows for the launch and recovery of a diverse spectrum of aircraft, including larger and more powerful jets, increasing operational flexibility and combat capability. The use of Electromagnetic Aircraft Launch Systems (EMALS) within CATOBAR is a crucial driver, providing more efficiency and less stress on airframes than traditional steam catapults. As countries such as China and India invest in carrier technology, the demand for CATOBAR systems increases, indicating a shift towards more complex naval operations.

Insights by Region

Get more details on this report -

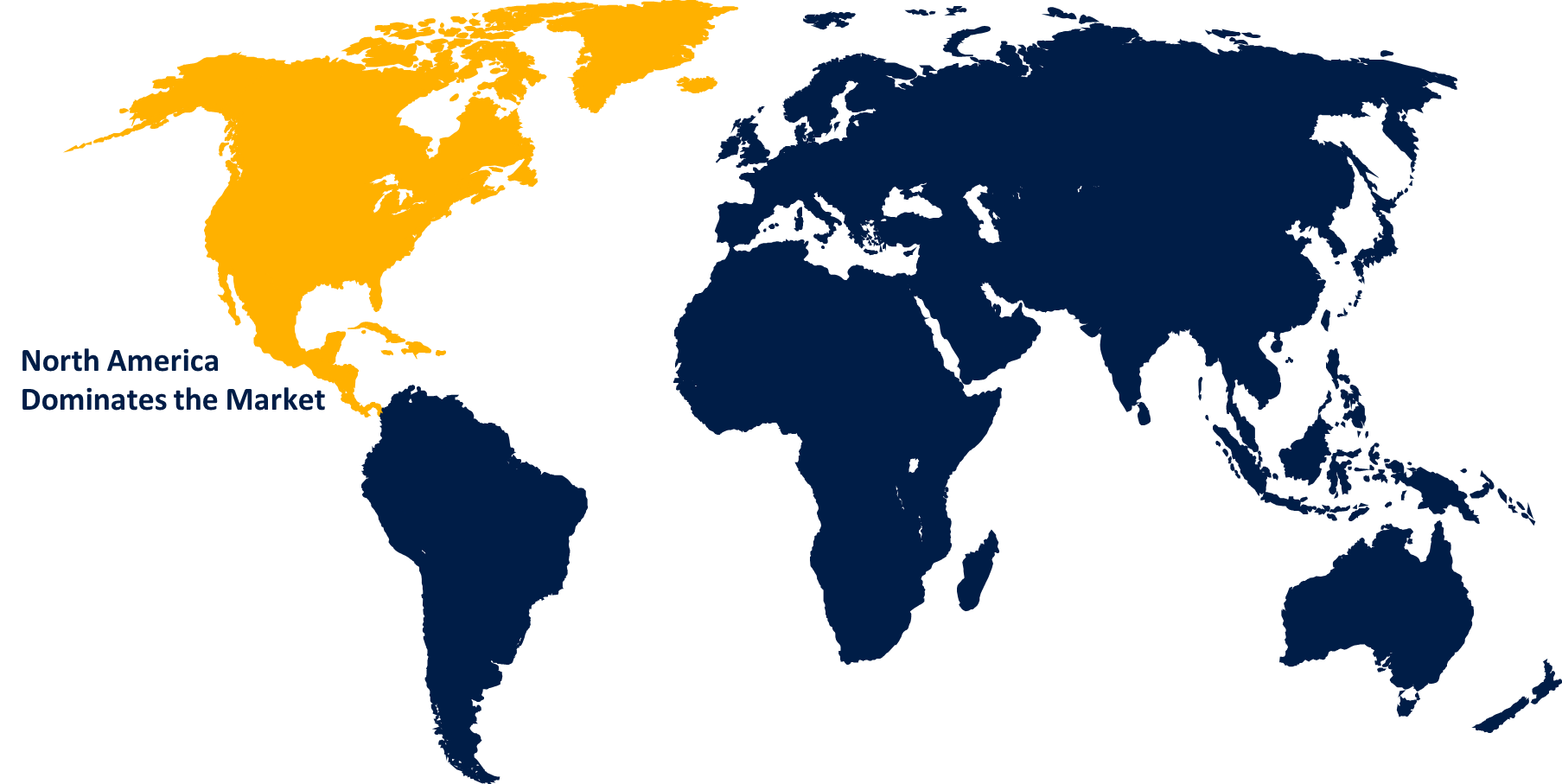

North America is anticipated to dominate the Aircraft Carrier Market from 2023 to 2033. Advanced technologies, including as nuclear propulsion, stealth features, and unmanned system integration, are being prioritised to improve operating efficiency and combat preparedness. The region benefits from strong defence budgets, which provide significant support for research, development, and procurement. Key players in carrier design and construction are Huntington Ingalls Industries and General Dynamics. Furthermore, government backing for strategic defence programs and partnerships boosts market growth. Despite problems such as high costs and long construction schedules, North America's aircraft carrier market remains a key component of global naval power.

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. Key countries such as China and India are leading the way, investing extensively in the development and modernisation of carrier fleets to improve maritime security and force projection. China's breakthroughs in carrier technology, especially the construction of domestically constructed carriers, demonstrate its strategic objectives. India, too, is focussing on indigenously manufactured carriers to boost its naval capability. The market benefits from regional partnerships as well as technological advancements in propulsion systems, avionics, and unmanned aerial vehicles.

Recent Market Developments

- In December 2020, The Indian government has announced its desire to acquire a third indigenous aircraft carrier-2 (IAC-2). This aircraft carrier is expected to be an enhanced variant of the INS Vikramaditya. The Indian government's second aircraft carrier, INS Vikrant (IAC-1), will enter service in 2022 following testing.

Major players in the market

- Lockheed Martin Corporation (The U.S.)

- BAE Systems PLC (The U.K.)

- Fincantieri SpA (Italy)

- General Dynamics Corporation (The U.S.)

- Huntington Ingalls Industries Inc. (The U.S.)

- Leonardo SpA (Italy)

- Navantia (Spain)

- Northrop Grumman Corporation (The U.S.)

- Thales Group (France)

- The Naval Group (France)

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Aircraft Carrier Market, Type Analysis

- Conventional-Powered

- Nuclear-Powered

Aircraft Carrier Market, Configuration Analysis

- Catapult-Assisted Take-Off but Arrested Recovery

- Short Take-Off but Arrested Recovery

- Short Take-Off but Vertical Recovery

Aircraft Carrier Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?