Global Automotive Simulation Market Size To Worth USD 6.2 Billion By 2033 | CAGR of 7.18%

Category: Automotive & TransportationGlobal Automotive Simulation Market Size To Worth USD 6.2 Billion By 2033

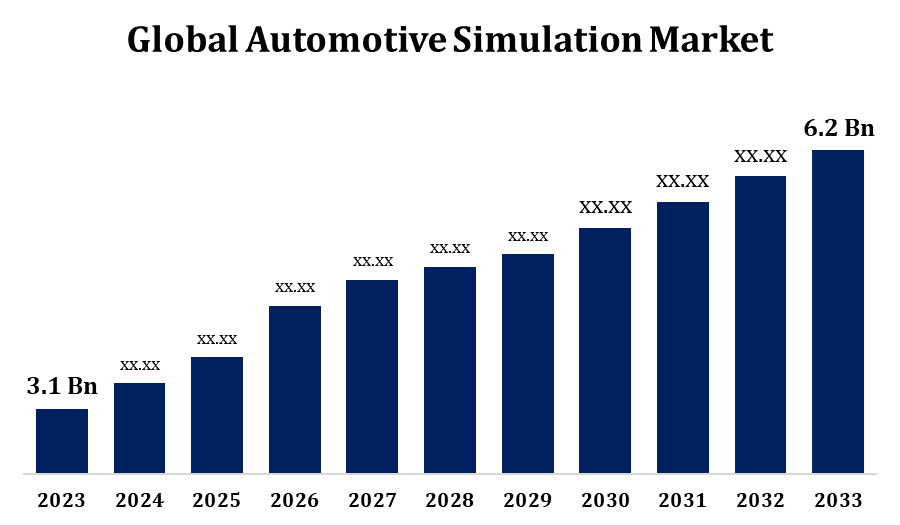

According to a research report published by Spherical Insights & Consulting, the Global Automotive Simulation Market Size to Grow from USD 3.1 Billion in 2023 to USD 6.2 Billion By 2033, at a Compound Annual Growth Rate (CAGR) of 7.18% during the Forecast Period.

Get more details on this report -

Browse key industry insights spread across 240 pages with 110 Market data tables and figures & charts from the report on the "Global Automotive Simulation Market Size, Share, and COVID-19 Impact Analysis, By Application (Drive Systems, Mechanical Components, and Fluid Power), By Deployment (On-premises and Cloud), By Component (Software and Services), By End users (OEM, Suppliers), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033." Get Detailed Report Description Here: https://www.sphericalinsights.com/reports/automotive-simulation-market

The automotive simulation market is expanding rapidly, driven by advancements in autonomous vehicles, electric mobility, and digital twin technology. Automakers and suppliers leverage simulation tools to improve vehicle design, safety testing, and performance optimization while minimizing costs and development time. Key applications include crash simulations, aerodynamics, powertrain efficiency, and driver assistance systems. The integration of artificial intelligence and machine learning enhances predictive analytics in vehicle simulations. Additionally, stringent safety and emissions regulations are increasing the demand for virtual testing. Industry leaders such as Siemens, Ansys, and Dassault Systèmes provide cutting-edge simulation solutions. The growing adoption of connected and software-defined vehicles is expected to drive further market expansion, supported by continuous technological advancements and the digital transformation of the automotive industry.

Automotive Simulation Market Value Chain Analysis

The automotive simulation market value chain comprises several key stages, from software development to end-user applications. It starts with software providers like Ansys, Siemens, and Dassault Systèmes, who create simulation tools for vehicle design, testing, and validation. Hardware providers supply high-performance computing systems to support complex simulations. Automakers and Tier 1 suppliers integrate these solutions to enhance vehicle performance, safety, and efficiency. Regulatory bodies play a vital role by establishing safety and emission standards that drive simulation adoption. Research institutions and testing labs contribute by refining models and ensuring accuracy. Finally, end-users, including OEMs, component manufacturers, and autonomous vehicle developers, apply these tools in real-world scenarios. The value chain is increasingly influenced by AI, digital twin technology, and cloud-based simulation platforms.

Automotive Simulation Market Opportunity Analysis

The automotive simulation market offers substantial growth opportunities, fueled by advancements in electric vehicles, autonomous driving, and connected car technologies. The increasing complexity of modern vehicles necessitates advanced simulation tools for virtual prototyping, crash testing, and real-time performance analysis, helping reduce costs and development time. AI and digital twin technology are enhancing predictive modeling, improving vehicle efficiency and safety. Stricter emissions and safety regulations are further driving demand for simulation solutions. Cloud-based platforms and high-performance computing are making these tools more accessible to small and mid-sized manufacturers. Additionally, the rapid adoption of simulation technologies in emerging Asia-Pacific markets is accelerating growth. As automakers transition to software-defined vehicles and over-the-air updates, the demand for sophisticated simulation tools is expected to rise, sustaining market expansion.

Technological advancements are driving growth in the automotive simulation market by improving vehicle design, safety, and performance optimization. The integration of artificial intelligence, digital twin technology, and high-performance computing allows automakers to conduct virtual prototyping, crash testing, and real-time performance analysis with greater accuracy and efficiency. The rising adoption of electric and autonomous vehicles is further boosting demand for simulation tools to test complex systems in a cost-effective and time-efficient manner. Cloud-based simulation platforms are increasing accessibility, helping manufacturers streamline development processes. Additionally, stringent emissions and safety regulations are reinforcing the need for advanced simulation solutions. As the industry moves toward software-defined vehicles and over-the-air updates, simulation technology continues to evolve, playing a vital role in driving innovation and market expansion.

Despite its rapid growth, the automotive simulation market faces several challenges. High initial investment costs for advanced simulation software and hardware can be a barrier, particularly for small and mid-sized manufacturers. Ensuring the accuracy and reliability of simulation models is complex, as real-world conditions are difficult to replicate. The integration of AI, machine learning, and digital twin technology requires specialized expertise, leading to a talent gap in the industry. As cloud-based and connected simulations become more widespread, cybersecurity concerns also emerge. Compliance with evolving safety and emission regulations adds complexity, necessitating frequent software updates. Additionally, interoperability between various simulation platforms and existing automotive systems remains a significant hurdle. Overcoming these challenges is crucial for maximizing the potential of automotive simulation technology.

Insights by Application

The drive systems segment accounted for the largest market share over the forecast period 2023 to 2033. Automakers are increasingly leveraging simulation tools to enhance powertrain efficiency, battery management, and thermal performance. As the industry shifts toward electrification, simulation software is essential for developing high-performance electric motors, inverters, and regenerative braking systems. Advanced simulation technologies enable manufacturers to cut costs, accelerate R&D, and optimize drivetrain components to improve vehicle range. The adoption of digital twin technology and AI-powered simulations is growing, facilitating real-time testing and predictive maintenance. With stricter global regulations on fuel efficiency and emissions, the demand for accurate and cost-effective drive system simulations is rising, further fueling market growth in the years ahead.

Insights by Deployment

The on-premises segment accounted for the largest market share over the forecast period 2023 to 2033. Many companies opt for on-premises solutions to retain full control over sensitive design and testing data, particularly in crash simulations, powertrain optimization, and ADAS development. This segment remains strong among large OEMs and Tier 1 suppliers that require robust simulation environments with minimal latency and high computational power. While cloud-based solutions are becoming more popular, on-premises systems are essential for managing complex simulations that require real-time processing and seamless integration with in-house hardware. As the automotive industry continues advancing vehicle technologies, the demand for secure, high-performance simulation infrastructure is expected to drive sustained growth in the on-premises segment.

Insights by Component

The service segment accounted for the largest market share over the forecast period 2023 to 2033. As simulation tools become increasingly essential for vehicle design, testing, and validation, companies rely on specialized services to enhance performance and meet evolving regulatory requirements. Service providers support customization of simulation models, offer cloud-based solutions, and maintain high-performance computing infrastructure. The growing adoption of electric vehicles, autonomous driving, and connected car technologies is further fueling demand for simulation-as-a-service, enabling cost-effective and scalable solutions. With a focus on reducing development cycles and improving efficiency, automotive firms are driving the need for consulting, technical support, and training services, making the service segment a vital contributor to overall market growth.

Insights by End Users

The suppliers segment accounted for the largest market share over the forecast period 2023 to 2033. With the growing adoption of electric vehicles, autonomous driving, and connected technologies, suppliers are utilizing simulation software to improve product performance, durability, and compliance with safety standards. Virtual prototyping facilitates cost-effective development of essential components such as batteries, sensors, powertrains, and braking systems, minimizing the need for physical testing. Digital twin technology and AI-driven simulations are further optimizing production processes and predictive maintenance. As OEMs push for faster innovation cycles and higher-quality components, suppliers are embracing advanced simulation solutions to enhance efficiency, remain competitive, and meet evolving regulatory and performance standards in the automotive industry.

Insights by Region

Get more details on this report -

North America is anticipated to dominate the Automotive Simulation Market from 2023 to 2033. The U.S. leads the market, driven by significant R&D investments, a strong automotive sector, and government regulations focused on vehicle safety and emissions reduction. The adoption of cloud-based simulation and digital twin technology is rising, enabling cost-effective and real-time testing. OEMs, suppliers, and mobility startups are increasingly utilizing simulation tools for virtual prototyping and crash testing. As the industry transitions to electric vehicles and connected cars, the demand for simulation software is expected to grow, accelerating safer and more efficient vehicle development.

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. China, Japan, and South Korea dominate the market, driven by strong automotive manufacturing, government support for EV adoption, and increasing investments in AI-powered simulation technologies. Automakers and suppliers utilize simulation software for vehicle design, crash testing, and performance optimization, helping reduce costs and development time. The adoption of digital twin technology and cloud-based simulations is expanding, enabling real-time data analysis and predictive maintenance. With the rise of connected vehicles and stricter safety regulations, demand for simulation solutions continues to grow. The increasing presence of global players, combined with domestic innovations, is expected to further accelerate the growth of the automotive simulation market in the region.

Recent Market Developments

- In January 2024, ANSYS, Inc. has announced that its AVxcelerate Sensors will be integrated into NVIDIA DRIVE Sim, a scenario-based autonomous vehicle (AV) simulator powered by NVIDIA Omniverse.

Major players in the market

- Altair Engineering, Inc.

- Autodesk Inc.

- ANSYS, Inc.

- PTC

- Dassault Systèmes

- The MathWorks, Inc.

- Rockwell Automation

- Simulations Plus

- ESI Group

- Applied Intuition, Inc.

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Automotive Simulation Market, Application Analysis

- Drive Systems

- Mechanical Components

- Fluid Power

Automotive Simulation Market, Deployment Analysis

- On-premises

- Cloud

Automotive Simulation Market, Component Analysis

- Software

- Services

Automotive Simulation Market, End Users Analysis

- OEM

- Suppliers

Automotive Simulation Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?