Global Semiconductor and IC Packaging Materials Market Size To Worth USD 10.2 Billion By 2033 | CAGR of 8.53%

Category: Semiconductors & ElectronicsGlobal Semiconductor and IC Packaging Materials Market Size To Worth USD 10.2 Billion By 2033

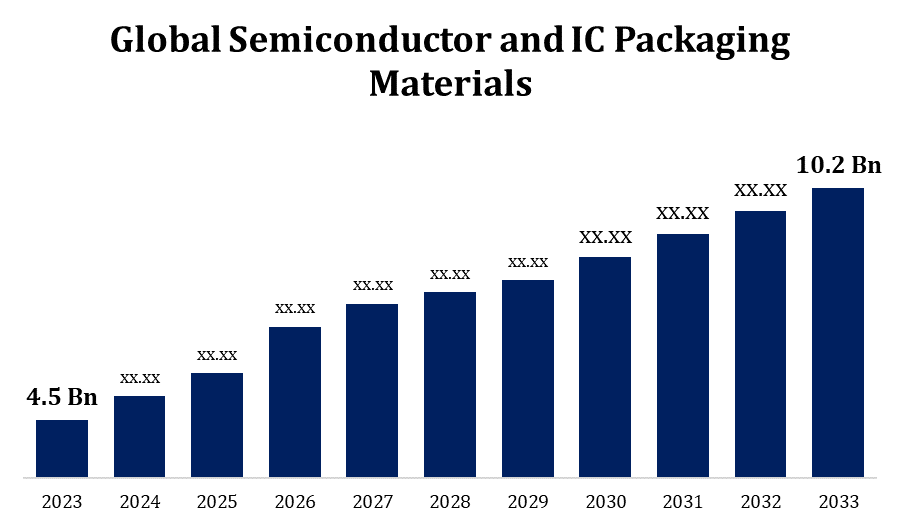

According to a research report published by Spherical Insights and Consulting, The Global Semiconductor and IC Packaging Materials Market Size to Grow from USD 4.5 Billion in 2023 to USD 10.2 Billion by 2033, at a Compound Annual Growth Rate (CAGR) of 8.53% during the forecast period.

Get more details on this report -

Browse key industry insights spread across 210 pages with 115 Market data tables and figures & charts from the report on the "Global Semiconductor and IC Packaging Materials Market Size, Share, and COVID-19 Impact Analysis, by Type (Organic substrate, Bonding wires, Leadframes, Encapsulation resins, Ceramic packages, Die attach materials, Solder balls), By End-user (Aerospace and Defence, Automotive, Consumer Electronics, Healthcare, IT and Telecommunication, Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033." Get Detailed Report Description Here: https://www.sphericalinsights.com/reports/semiconductor-and-ic-packaging-materials-market

The semiconductor and IC packaging materials market is crucial for meeting the miniaturization and performance requirements of modern electronics. This sector includes essential materials such as organic substrates, lead frames, bonding wires, encapsulants, and solder balls, which protect, connect, and optimize integrated circuits (ICs) in various devices. The rising demand for high-performance products, including smartphones, automotive electronics, and IoT devices, propels market growth. Advanced packaging methods, like 3D stacking and fan-out wafer-level packaging, necessitate specialized materials that enhance thermal management, minimize size, and improve energy efficiency. The Asia-Pacific region, home to major semiconductor manufacturers, leads the market, while trends toward sustainability drive the need for eco-friendly materials. As technology advances, this sector is poised for significant growth, spurring innovations in consumer electronics, AI, and data centers.

Semiconductor and IC Packaging Materials Market Value Chain Analysis

The value chain of the semiconductor and IC packaging materials market encompasses multiple stages, beginning with raw material sourcing and extending to end-user applications. Initially, suppliers deliver critical raw materials such as metals, ceramics, and polymers to manufacturers who create substrates, bonding wires, encapsulants, and lead frames. These components are then supplied to IC packaging companies, which utilize them in advanced packaging solutions like flip-chip, 3D packaging, and fan-out wafer-level packaging. Quality assurance and compliance are upheld by testing and inspection firms throughout the process, ensuring reliability for performance-sensitive applications. Distributors and vendors play a vital role in the global supply of these materials, particularly in high-demand regions like Asia-Pacific. End-users across the electronics, automotive, and telecommunications sectors depend on these materials to achieve miniaturization, enhance thermal management, and improve power efficiency in their final products.

Semiconductor and IC Packaging Materials Market Opportunity Analysis

The semiconductor and IC packaging materials market is poised for substantial growth, propelled by trends such as 5G, IoT, AI, and automotive electrification. As devices become increasingly compact and powerful, the demand for advanced packaging materials that enhance thermal management, electrical performance, and reliability continues to rise. Emerging technologies like 3D packaging and fan-out wafer-level packaging require specialized materials, creating opportunities for innovation. The movement towards sustainable and eco-friendly materials presents additional prospects, as both regulatory bodies and end-users prioritize greener alternatives. Moreover, the growing semiconductor manufacturing base in the Asia-Pacific region further drives demand, establishing it as a key area for growth. Companies that focus on RandD for high-performance materials and sustainable manufacturing practices are well-positioned to gain a competitive advantage in this rapidly evolving market.

The growing significance of semiconductors in industrial automation is a major factor driving growth in the semiconductor and IC packaging materials market. Technologies such as robotics, artificial intelligence, and machine learning increasingly depend on high-performance semiconductors for real-time data processing, predictive maintenance, and precise control systems. As industries advance, the demand for sophisticated semiconductor packaging materials—especially those that improve durability, thermal management, and power efficiency—rises to meet the needs of high-stress, high-temperature environments. Innovations such as System-in-Package (SiP) and fan-out wafer-level packaging facilitate the integration of multiple components into compact modules, which are essential for IoT devices and edge computing in automation. As industrial automation continues to accelerate across sectors like manufacturing, logistics, and energy, the demand for specialized semiconductor packaging materials is anticipated to grow significantly, driving overall market expansion.

Supply chain disruptions, especially in the sourcing of raw materials, can result in production delays and cost fluctuations, negatively impacting profitability. Additionally, the industry confronts technical challenges as devices increasingly require more intricate packaging solutions, such as 3D stacking and fan-out wafer-level packaging, which demand advanced materials with superior performance and durability. Growing environmental concerns are also significant, as traditional materials frequently contain non-biodegradable and toxic components, pushing companies to seek sustainable alternatives. The high research and development costs associated with creating new, eco-friendly, high-performance materials place an additional financial burden on smaller manufacturers. Furthermore, regional regulations regarding electronic waste and emissions impose further compliance challenges, necessitating innovation while balancing cost-efficiency and sustainability.

Insights by Type

The organic substrate segment accounted for the largest market share over the forecast period 2023 to 2033. Organic substrates, primarily composed of materials like epoxy resin and polyimide, offer a cost-effective yet high-performance solution for interconnecting and supporting integrated circuits. These substrates exhibit excellent thermal and electrical characteristics, making them well-suited for high-density applications in smartphones, automotive electronics, and IoT devices. As the need for miniaturization and multifunctionality in electronic devices grows, organic substrates are essential for enabling compact designs while ensuring reliability. The increasing demand for 5G, AI, and wearable technologies further drives the need for organic substrates, as they deliver the necessary adaptability, insulation, and structural integrity required for these next-generation applications.

Insights by End User

The IT and telecommunication segment accounted for the largest market share over the forecast period 2023 to 2033. Growth in this sector is driven by the rapid expansion of 5G networks, cloud computing, and data centers. As the demand for faster data transmission, increased processing speeds, and reliable connectivity rises, the industry heavily depends on advanced packaging materials that enhance performance, minimize latency, and facilitate miniaturization. Essential materials, such as organic substrates, bonding wires, and encapsulants, are critical for high-performance packaging solutions like flip-chip and fan-out wafer-level packaging. The rising prevalence of mobile devices, IoT, and AI applications further intensifies the demand for robust and efficient packaging solutions to address power and thermal management challenges. Ongoing investments in 5G infrastructure and digital transformation are expected to sustain growth in semiconductor packaging materials within the IT and telecom sectors.

Insights by Region

Get more details on this report -

North America is anticipated to dominate the Semiconductor and IC Packaging Materials Market from 2023 to 2033. Key industries such as automotive, aerospace, and consumer electronics are driving the demand for high-performance semiconductors, which in turn increases the need for specialized packaging materials that improve durability, thermal management, and miniaturization. North America is home to prominent semiconductor companies and research institutions, fostering innovation in packaging techniques like 3D integration and fan-out wafer-level packaging. With the expansion of 5G, IoT, and AI applications, there is a growing demand for high-density and reliable packaging solutions in the region. Additionally, government initiatives aimed at bolstering domestic semiconductor production and reducing dependence on imports present further market opportunities. Trends toward sustainability also promote the use of eco-friendly materials, influencing future growth in North America's semiconductor packaging materials market.

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. The region is a significant producer of semiconductors, supported by extensive supply chains and government backing. The rapid adoption of advanced technologies such as 5G, IoT, and AI drives the need for sophisticated packaging solutions that enhance device performance, reduce size, and improve energy efficiency. There is substantial adoption of advanced packaging technologies, including flip-chip, wafer-level, and 3D packaging, which increases the demand for specialized materials like substrates, bonding wires, and encapsulants. Moreover, Asia-Pacific's focus on cost-effective production and high-volume manufacturing attracts global investments, reinforcing its status as a key growth area for semiconductor packaging materials, particularly as companies pursue sustainable and high-performance solutions.

Recent Market Developments

- On June 2024, Shin-Etsu Chemical has introduced new equipment for producing semiconductor package substrates through the dual damascene method. This innovation eliminates the necessity for interposers, reducing production costs and allowing for more precise microfabrication in advanced semiconductor assembly.

Major players in the market

- DuPont

- Henkel

- Hitachi High-Tech

- Samsung Electro-Mechanics

- Shin-Etsu Chemical

- Sumitomo Chemical

- Texas Instruments

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Semiconductor and IC Packaging Materials Market, Type Analysis

- Organic substrate

- Bonding wires

- Leadframes

- Encapsulation resins

- Ceramic packages

- Die attach materials

- Solder balls

Semiconductor and IC Packaging Materials Market, End User Analysis

- Aerospace and Defence

- Automotive

- Consumer Electronics

- Healthcare

- IT and Telecommunication

- Others

Semiconductor and IC Packaging Materials Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East and Africa

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?