Global Shipbuilding Market Size To Exceed USD 210.13 Billion By 2033 | CAGR of 3.91%

Category: Automotive & TransportationGlobal Shipbuilding Market Size To Exceed USD 210.13 Billion By 2033

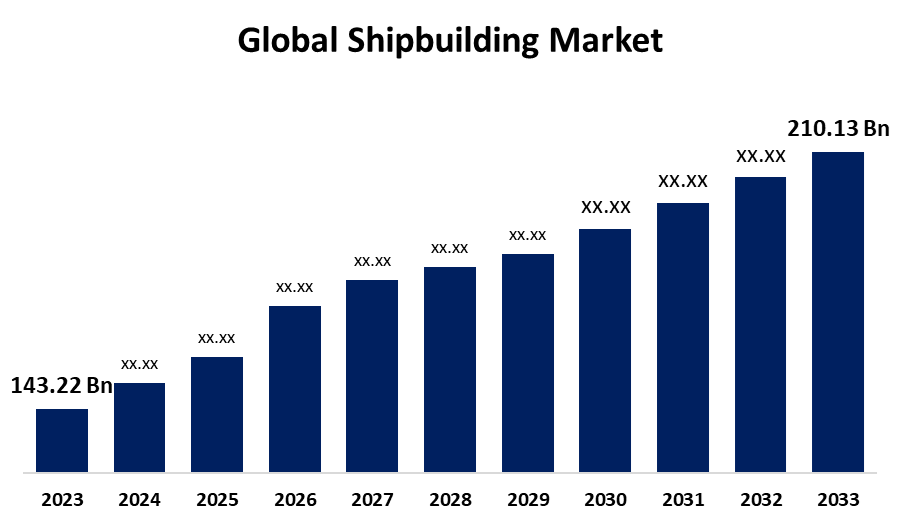

According to a research report published by Spherical Insights & Consulting, the Global Shipbuilding Market Size is Expected to Grow from USD 143.22 Billion in 2023 to USD 210.13 Billion by 2033, at a CAGR of 3.91% during the forecast period 2023-2033.

Get more details on this report -

Browse key industry insights spread across 210 pages with 115 Market data tables and figures & charts from the report on the "Global Shipbuilding Market Size, Share, and COVID-19 Impact Analysis, By Type (Vessel, Container, and Passenger), By End User (Transport Companies and Military), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 – 2033."Detailed Report Description Here:https://www.sphericalinsights.com/reports/shipbuilding-market

In the shipbuilding industry, massive floating ships or vessels are built using steel, wood, and several other materials. This market encompasses a variety of ship types, including military ships, leisure ships (such as yachts and cruise ships), and commercial ships (such as tankers and cargo ships). In addition to shipyards and other establishments where ships are built and maintained, the market also comprises providers of the components, materials, and technology used in shipbuilding. Additionally, the expansion of trade agreements among several nations is contributing to the growth and development of the global shipbuilding market. Furthermore, the number of ships in the globe is growing, including commercial, cruise, and other types, which will raise demand for shipbuilding and maintenance services. In total, there were 102,899 seagoing commercial ships. The expanding worldwide fleet of vessels is fueling further market expansion and growth in the projected period. Additionally, the global shipbuilding industry received contracts totaling 65.8 million compensated gross tonnes (CGT) in 2024. Throughout the year, orders of about 22.8 million CGT, or 45.7 million CGT, were placed with Chinese shipbuilders. The growing number of contracts in the shipbuilding sector is one motivating aspect that propels market expansion. However, the shipbuilding industry is very cyclical, going through phases of expansion and contraction. Changes in shipbuilding orders, the state of the economy, and the volatility of the financial markets can all lead to periods of overcapacity. During times of overcapacity, shipbuilding firms face intense competition, price pressure, and reduced profit margins.

The vessel segment accounted for the largest share in 2023 and is expected to grow at a significant CAGR during the forecast period.

Based on the type, the shipbuilding market is classified into vessel, container, and passenger. Among these, the vessel segment accounted for the largest share in 2023 and is expected to grow at a significant CAGR during the forecast period. Bulk carriers move dry and loose commodities such as coal, cement, ores, cereal grains, and other items. Since these commodities don't need special packaging, the dry bulk freight charges have remained the same, allowing for more flexibility throughout the major economies.

The transport companies segment accounted for the largest share in 2023 and is expected to grow at a significant CAGR during the forecast period.

Based on the end user, the shipbuilding market is divided into transport companies and military. Among these, the transport companies segment accounted for the largest share in 2023 and is expected to grow at a significant CAGR during the forecast period. A large percentage of the shipbuilding industry is controlled by transport companies as a result of the expanding demand from the logistics and freight industries.

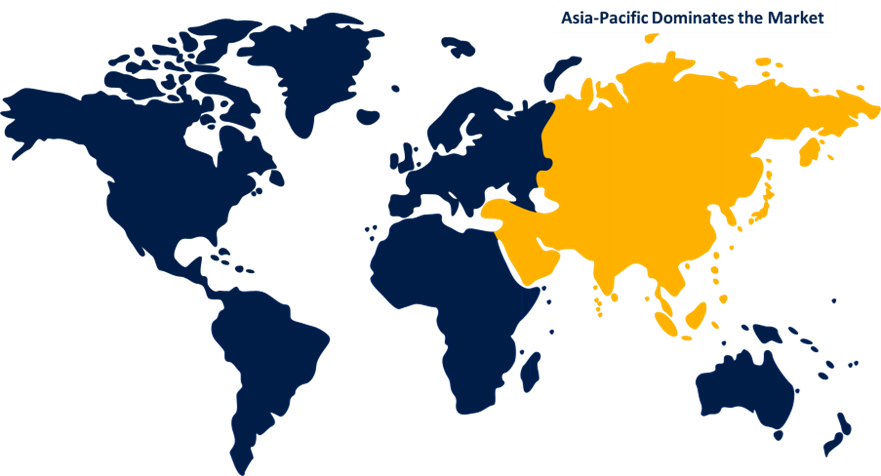

Asia Pacific is estimated to hold the largest share of the shipbuilding market over the forecast period.

Get more details on this report -

Asia Pacific is estimated to hold the largest share of the shipbuilding market over the forecast period. The top three countries in the Asia Pacific shipbuilding industry are China, South Korea, and Japan. They have developed into significant shipbuilding hubs due to their infrastructure, cost advantages, and technological know-how. The region has a significant demand for offshore support boats, commercial ships, and naval ships. In terms of delivery orders and order books, China has a significant market share of 43.1%, 48.8%, and 44.7% of the worldwide market, according to the Ministry of Industry and Information Technology (MIIT).

North America is predicted to have the fastest CAGR growth in the shipbuilding market over the forecast period. The US shipbuilding industry has been losing ground as a result of several causes, including a decline in federal cargo, intense overseas competition supported by government subsidies, and commercial ship orders. The domestic shipbuilding sector, which includes approximately 120 shipyards in the United States, currently has the government as its primary client.

Major key players in the shipbuilding market are Mitsubishi Heavy Industries Ltd., Hyundai Heavy Industries Co. Ltd., China State Shipbuilding Corporation, Daewoo Shipbuilding & Marine Engineering Co. Ltd., Samsung Heavy Industries, Sumitomo Heavy Industries, Hanjin Heavy Industries and Construction Co., Yangzijiang Shipbuilding Ltd., United Shipbuilding Corporation, STX Group, and others.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Key Market Developments

- In June 2024, the Portland Harbour Authority (PHA) in the United Kingdom has contracted with Damen Shipyards to supply Damen ASD Tug 2111, one of its newest tugs. The 21-meter-long and extremely nimble ASD Tug 2111 can tow 50 tons of bollards.

Market Segment

This study forecasts global, regional, and country revenue from 2023 to 2033. Spherical Insights has segmented the shipbuilding market based on the below-mentioned segments:

Global Shipbuilding Market, By Type

- Vessel

- Container

- Passenger

Global Shipbuilding Market, By End User

- Transport Companies

- Military

Global Shipbuilding Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?