Global Software Defined Vehicle Market Size To Worth USD 1849.6 Billion By 2033 | CAGR of 18.26%

Category: Automotive & TransportationGlobal Software Defined Vehicle Market Size To Worth USD 1849.6 Billion By 2033

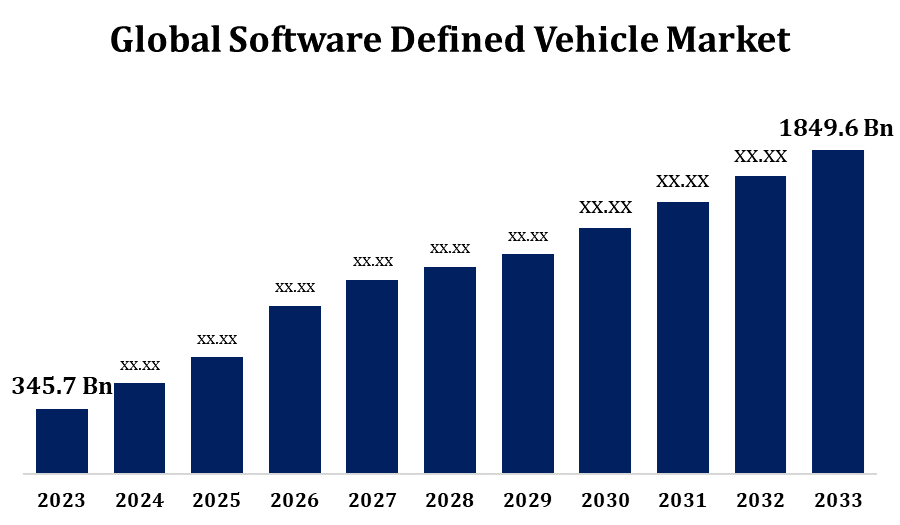

According to a research report published by Spherical Insights & Consulting, the Global Software Defined Vehicle Market Size to grow from USD 345.7 billion in 2023 to USD 1849.6 billion by 2033, at a Compound Annual Growth Rate (CAGR) of 18.26% during the forecast period.

Get more details on this report -

Browse key industry insights spread across 220 pages with 115 Market data tables and figures & charts from the report on the "Global Software Defined Vehicle Market Size, Share, and COVID-19 Impact Analysis, By Offering (Hardware, Software and Services), By Vehicle Type (ICE, BEV, HEV/PHEV), By Application (Powertrain & Chassis, ADAS/HAD, Body and Energy, Infotainment, and Connectivity & Security), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033." Get Detailed Report Description Here: https://www.sphericalinsights.com/reports/software-defined-vehicle-market

The Software-Defined Vehicle market is experiencing rapid expansion, driven by advancements in automotive electronics, connectivity, and artificial intelligence. These vehicles utilize software-centric architectures that support over-the-air updates, enhanced safety features, and autonomous driving capabilities. Automakers are transitioning from traditional hardware-focused designs to flexible, software-driven models, enabling continuous improvements and personalized user experiences. Leading companies such as Tesla, Volkswagen, and General Motors are investing in software-defined platforms to enhance performance and security. The growing adoption of electric vehicles and fifth-generation mobile networks further accelerates market growth. However, challenges such as cybersecurity risks, high development costs, and regulatory requirements persist. Despite these obstacles, rising consumer demand for smart mobility and strategic collaborations between technology firms and automakers are driving the market forward, positioning Software-Defined Vehicles as the future of the automotive industry.

Software Defined Vehicle Market Value Chain Analysis

The Software-Defined Vehicle market value chain comprises several key segments, including semiconductor manufacturers, software developers, automakers, and service providers. It begins with chipmakers like Nvidia, Qualcomm, and Intel, which supply high-performance computing hardware. Software providers such as BlackBerry QNX, Android Automotive, and AUTOSAR develop operating systems, middleware, and artificial intelligence-driven applications. Automakers like Tesla, BMW, and Ford integrate these software solutions into vehicle architectures, enabling over-the-air updates, autonomous capabilities, and connected services. Cloud and connectivity providers, including Amazon Web Services, Microsoft Azure, and fifth-generation mobile network operators, ensure efficient data management and vehicle-to-everything communication. Tier-1 suppliers like Bosch and Continental bridge hardware and software integration. Additionally, service providers offer cybersecurity, data analytics, and subscription-based features. Strong collaboration across these segments is essential for driving innovation, security, and scalability in the evolving Software-Defined Vehicle landscape.

Software Defined Vehicle Market Opportunity Analysis

The Software-Defined Vehicle market offers substantial opportunities fueled by advancements in connectivity, artificial intelligence, and cloud computing. Increasing demand for over-the-air updates, autonomous driving, and personalized in-car experiences is prompting automakers to embrace software-centric architectures. The transition to electric vehicles further amplifies the need for software-driven solutions to enhance energy efficiency and performance. Technology companies can leverage opportunities in cybersecurity, data analytics, and vehicle-to-everything communication. Additionally, regulatory initiatives promoting safer and smarter mobility create a conducive environment for innovation. Emerging revenue streams include subscription-based software services, digital twin technology, and predictive maintenance solutions. Collaboration among automakers, semiconductor manufacturers, and software providers will be crucial in realizing the full potential of this market, positioning Software-Defined Vehicles as a key driver of the automotive industry’s future.

The Software-Defined Vehicle market is expanding as modern vehicles increasingly integrate advanced technologies. Automakers are shifting from conventional hardware-based designs to software-centric architectures, enabling real-time updates, enhanced automation, and improved performance. The adoption of artificial intelligence, machine learning, and cloud computing facilitates seamless over-the-air updates, predictive maintenance, and advanced driver assistance systems. Innovations in connectivity, including fifth-generation mobile networks and vehicle-to-everything communication, further drive market growth. Additionally, the transition to electric vehicles increases the demand for intelligent software solutions to optimize energy management and enhance the overall user experience.

A key challenge in the Software-Defined Vehicle market is cybersecurity, as greater connectivity and over-the-air updates increase the risk of hacking and data breaches. The high cost of software development and integration also presents obstacles, requiring substantial investment in advanced computing hardware and cloud infrastructure. Ensuring seamless compatibility between software and vehicle hardware remains complex, necessitating close collaboration between automakers, technology providers, and semiconductor manufacturers. Regulatory compliance adds another layer of difficulty, as safety and data privacy laws continue to evolve across different regions. Additionally, the demand for continuous software updates and maintenance introduces operational complexities for automakers, requiring robust infrastructure and long-term support strategies.

Insights by Offering

The software segment accounted for the largest market share over the forecast period 2023 to 2033. The growing demand for over-the-air updates, artificial intelligence-powered systems, and autonomous driving is driving the advancement of sophisticated operating systems, middleware, and cloud-based services. Leading providers such as BlackBerry QNX, Android Automotive, and AUTOSAR are developing secure and scalable software platforms. The increasing adoption of electric vehicles further amplifies the need for intelligent software to enhance battery performance and energy management. Additionally, subscription-based software services, digital twin technology, and predictive maintenance solutions are unlocking new revenue opportunities for automakers. As vehicles become increasingly software-centric, the software segment will remain a key driver of innovation and market growth.

Insights by Vehicle Type

The BEV segment accounted for the largest market share over the forecast period 2023 to 2033. Automakers like Tesla, BYD, and Volkswagen are incorporating advanced software to optimize battery efficiency, enable real-time diagnostics, and support over-the-air updates. Intelligent energy management systems and artificial intelligence-driven predictive maintenance further enhance vehicle durability and the overall user experience. Additionally, the expansion of charging infrastructure and vehicle-to-grid technology is enabling seamless integration with smart grids. As governments worldwide promote electric mobility through incentives and stricter emissions regulations, the demand for software-driven electric vehicles continues to grow. The fusion of electric and software-defined technologies is reshaping the automotive industry, positioning battery electric vehicles as a crucial segment in the future of mobility.

Insights by Application

The ADAS/HAD segment accounted for the largest market share over the forecast period 2023 to 2033. Automakers are increasingly leveraging artificial intelligence, machine learning, and sensor fusion technologies to enhance vehicle safety, automation, and user experience. Features such as adaptive cruise control, lane-keeping assist, and automated emergency braking are becoming standard in Advanced Driver Assistance Systems, while Highly Automated Driving is steadily advancing toward full autonomy. Companies like Tesla, Waymo, and Mercedes-Benz are investing in real-time data processing, over-the-air updates, and vehicle-to-everything communication to enhance automation capabilities. The growth of fifth-generation mobile networks and edge computing further enables low-latency decision-making. As regulatory frameworks evolve to support higher levels of automation, the Advanced Driver Assistance Systems and Highly Automated Driving segment will remain a key driver of growth in the Software-Defined Vehicle market.

Insights by Region

Get more details on this report -

North America is anticipated to dominate the Software Defined Vehicle Market from 2023 to 2033. The market is fueled by rapid technological advancements, growing consumer demand for connected vehicles, and the presence of leading automotive and technology companies. Automakers like Tesla, General Motors, and Ford are making significant investments in software-driven vehicle architectures, enabling over-the-air updates, autonomous driving, and advanced driver assistance systems. The region’s strong fifth-generation mobile network infrastructure and cloud computing capabilities further support the expansion of Software-Defined Vehicles. Additionally, regulatory initiatives focused on vehicle safety, emissions reduction, and smart mobility are accelerating market growth. Strategic collaborations among automakers, semiconductor manufacturers, and software providers are playing a vital role in shaping the future of the Software-Defined Vehicle market in North America.

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. China, Japan, and South Korea are leading the way, with automakers such as Toyota, Hyundai, and BYD investing in software-centric vehicle architectures. The rapid expansion of electric vehicles and autonomous driving technologies is further driving market adoption. Additionally, the presence of top semiconductor manufacturers and cloud service providers is advancing vehicle connectivity and artificial intelligence integration. Strong collaboration between automakers, technology companies, and government organizations is crucial for the continued development of Software-Defined Vehicles in the Asia-Pacific region, positioning it as a key player in the future growth of the industry.

Recent Market Developments

- In November 2024, Panasonic Automotive Systems Co., Ltd. partnered with Arm to develop a standardized automotive architecture for Software-Defined Vehicles.

Major players in the market

- Robert Bosch GmbH

- Nvidia Corporation

- Qualcomm Technologies Inc.

- Marelli Holdings Co., Ltd.

- Continental AG

- Volkswagen Group

- Harman International

- Tesla

- Volvo Group

- Ford Motor Company

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Software Defined Vehicle Market, Offering Analysis

- Hardware

- Software

- Services

Software Defined Vehicle Market, Vehicle Type Analysis

- ICE

- BEV

- HEV/PHEV

Software Defined Vehicle Market, Application Analysis

- Powertrain & Chassis

- ADAS/HAD

- Body and Energy

- Infotainment

- Connectivity & Security

Software Defined Vehicle Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?