Global 5G Substrate Materials Market Size, Share, and COVID-19 Impact Analysis, By Substrate Type (Organic Laminates, Ceramics, Glass, Others), By Application (Base Station Antennas, Smartphone Antennas, Electronics, Aerospace, Automobile), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033.

Industry: Advanced MaterialsGlobal 5G Substrate Materials Market Insights Forecasts to 2033

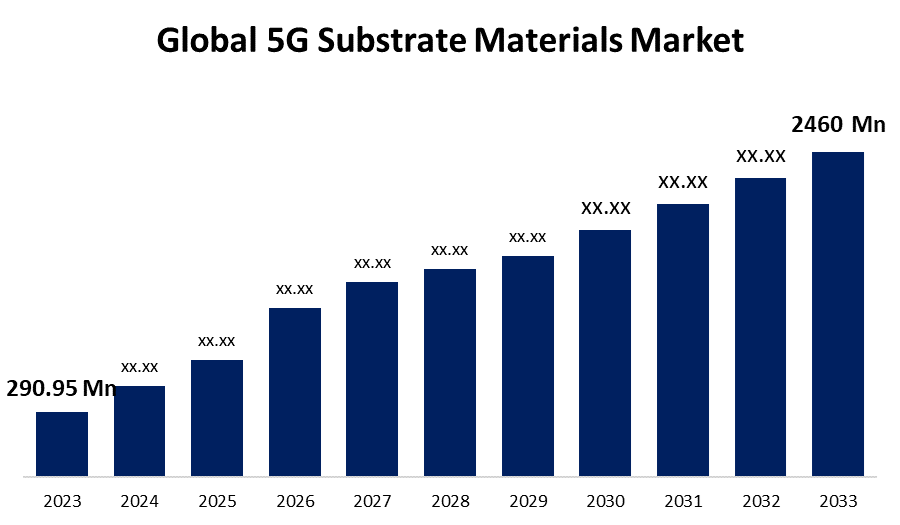

- The Global 5G Substrate Materials Market Size was Valued at USD 290.95 Million in 2023

- The Market Size is Growing at a CAGR of 23.80% from 2023 to 2033

- The Worldwide 5G Substrate Materials Market Size is Expected to Reach USD 2460 Million by 2033

- Aisa Pacific is Expected to Grow the fastest during the forecast period.

Get more details on this report -

The Global 5G Substrate Materials Market Size is Anticipated to Exceed USD 2460 Million by 2033, Growing at a CAGR of 23.80% from 2023 to 2033.

Market Overview

5G substrate materials refer to the types of materials used in the construction of electronic components and devices that support 5G wireless communication technologies. These materials are crucial for ensuring the performance, efficiency, and reliability of 5G infrastructure. Fifth Generation (5G) is the most recent communication backbone, enabling transformative industrial, medical, automotive, and defense applications. 5G offers numerous advantages, including increased speed (ten times faster than 4G), lower latency (at least ten times lower than 4G), and density (supporting around one million Internet of Things (IoT) devices per square kilometer). 5G technology will improve the overall security, dependability, service quality, and efficiency of the devices. The rising demand for 5G substrate materials from numerous industries, including automobile radars, 5G base station antennas, and smartphone antennas, has had a significant impact on the market's growth. Additionally, the rapid increase in the number of R&D projects and increasing demand for smartphones are also a key determinant influencing the growth of the 5G substrate materials market.

Report Coverage

This research report categorizes the market for 5G substrate materials market based on various segments and regions forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the 5G substrate materials market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the 5G substrate materials market.

Global 5G Substrate Materials Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 290.95 Million |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | CAGR of 23.80% |

| 2033 Value Projection: | USD 2460 Million |

| Historical Data for: | 2019 - 2022 |

| No. of Pages: | 269 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Substrate Type, By Application, By Region |

| Companies covered:: | 3M Company, Asahi Glass Company (AGC) Inc., DuPont de Nemours Inc., Kaneka Corporation, Taiwan Union Technology Corporation, Ventec International Group, Daikin Industries, Showa Denko Materials Co. Ltd., Kuraray Co. Ltd., Panasonic Corporation, Sumitomo Chemical Co. Ltd., The Chemours Company, Toray Industries Inc., Others, and |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The market for 5G substrate materials is driven by several key factors shaping its growth and development. Firstly, the demand for materials capable of supporting higher frequencies and data rates is essential for faster and more reliable communication in 5G networks Industry collaboration and partnerships between telecommunications firms, technology developers, and substrate material suppliers stimulate innovation and expedite the commercialization of 5G technologies. Furthermore, technological advancements in semiconductor manufacturing, enable the development of materials that can support higher frequencies, facilitate miniaturization, ensure high performance and reliability, cater to emerging applications, and meet the global demand for 5G infrastructure. Additionally, government initiatives, regulatory policies promoting 5G deployment, and increasing investments in communication infrastructure globally contribute significantly to the expansion of the substrate materials market.

Restraining Factors

The growth of the 5G substrate materials market is tempered by several significant restraining factors including high costs associated with advanced materials like high-frequency laminates and specialized ceramics present barriers to widespread adoption, particularly in cost-sensitive markets. Complex manufacturing processes and supply chain challenges further complicate scalability and affordability, while technological compatibility issues and regulatory compliance requirements add layers of complexity and cost. Additionally, market fragmentation and intense competition among suppliers contribute to pricing pressures and margin constraints.

Market Segmentation

The 5G substrate materials market share is classified into substrate type and application.

- The organic laminates segment is estimated to hold the highest market revenue share through the projected period.

Based on the substrate type, the 5G substrate materials market is classified into organic laminates, ceramics, glass, and others. Among these, the organic laminates segment is estimated to hold the highest market revenue share through the projected period. The organic laminates segment is dominated by their cost-effectiveness, compatibility with standard PCB manufacturing processes, and versatility in meeting the diverse needs of 5G infrastructure components. Organic laminates offer manufacturers and developers a balance of performance, manufacturability, and affordability crucial for widespread adoption across various applications including base stations, antennas, RF filters, and IoT devices.

- The base station antennas segment is anticipated to hold the largest market share through the forecast period.

Based on the application, the 5G substrate materials market is divided into base station antennas, smartphone antennas, electronics, aerospace, and automobile. Among these, the base station antenna segment is anticipated to hold the largest market share through the forecast period. This leadership is driven by the essential role of base stations in the expansion of 5G networks worldwide. Base station antennas serve as foundational components of telecommunications infrastructure, facilitating high-speed data transmission across various environments. The segment's prominence is bolstered by substantial investments in 5G infrastructure, necessitating large quantities of high-performance substrate materials such as ceramics and specialized laminates. These materials are essential for meeting the stringent requirements of high-frequency operation, low signal loss, and robust mechanical stability demanded by base station antennas.

Regional Segment Analysis of the 5G Substrate Materials Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the 5G substrate materials market over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the largest share of the 5G substrate materials market over the predicted timeframe. The region is attributed to the strong technological ecosystem, including leading telecommunications companies, technology innovators, and research institutions focused on advancing 5G infrastructure. This leadership position is reinforced by substantial investments in telecommunications infrastructure and favorable regulatory frameworks that support the rapid expansion of 5G networks. These factors collectively contribute to the high demand for advanced substrate materials essential for base stations, antennas, and other critical components of 5G networks.

Asia Pacific is expected to grow at the fastest CAGR growth of the 5G substrate materials market during the forecast period. The region's attributed to 5G technology adoption and infrastructure development. Countries like China, South Korea, and Japan are at the forefront of deploying 5G networks, fueled by large-scale investments in telecommunications infrastructure and strong government support. Asia Pacific hosts leading technology firms and manufacturers specializing in advanced telecommunications equipment and electronic components, facilitating continuous innovation in high-performance substrate materials essential for 5G applications. Rising consumer demand for enhanced mobile connectivity, faster internet speeds, and emerging technologies such as IoT further propel the expansion of 5G networks across the region.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the 5G substrate materials market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- 3M Company

- Asahi Glass Company (AGC) Inc.

- DuPont de Nemours Inc.

- Kaneka Corporation

- Taiwan Union Technology Corporation

- Ventec International Group

- Daikin Industries

- Showa Denko Materials Co. Ltd.

- Kuraray Co. Ltd.

- Panasonic Corporation

- Sumitomo Chemical Co. Ltd.

- The Chemours Company

- Toray Industries Inc.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In July 2024, Atomera introduced a new MST technology to improve RF-SOI wafer substrates, which is essential for 5G and 6G technologies. This method exhibited on 300mm RF-SOI wafers with an ultra-thin active layer, is intended to improve RF switches and low-noise amplifiers.

- In May 2024, DuPont announced that it will exhibit its entire spectrum of advanced circuit materials and solutions at the 2024 International Electronic Circuits Exhibition in Shanghai.

- In September 2023, Intel introduced one of the industry's first glass substrates for next-generation advanced packaging, which is set to launch later this decade. This groundbreaking discovery will allow for further scaling of transistors in a package, advancing Moore's Law and delivering data-centric applications.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2023 to 2033. Spherical Insights has segmented the 5G substrate materials market based on the below-mentioned segments:

Global 5G Substrate Materials Market, By Substrate Type

- Organic Laminates

- Ceramics

- Glass

- Others

Global 5G Substrate Materials Market, By Application

- Base Station Antennas

- Smartphone Antennas

- Electronics

- Aerospace

- Automobile

Global 5G Substrate Materials Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1.What is the CAGR of the 5G substrate materials market over the forecast period?The 5G substrate materials market is projected to expand at a CAGR of 23.80% during the forecast period.

-

2.What is the market size of the 5G substrate materials market?The Global 5G Substrate Materials Market Size is Expected to Grow from USD 290.95 Million in 2023 to USD 2460 Million by 2033, at a CAGR of 23.80% during the forecast period 2023-2033.

-

3.Which region holds the largest share of the 5G substrate materials market?North America is anticipated to hold the largest share of the 5G substrate materials market over the predicted timeframe.

Need help to buy this report?