Global Agriculture Supply Chain Management Market Size, Share, and COVID-19 Impact Analysis, By Component (Hardware, Solutions, and Services), By Solution (Manufacturing Execution System, Procurement & Sourcing, Transportation Management System, Supply Chain Planning, and Warehouse Management System), By Deployment (On-Demand & Cloud-Based, and On-Premise), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033Global Agriculture Supply Chain Management Market Insights Forecasts to 2033

Industry: AgricultureGlobal Agriculture Supply Chain Management Market insights Forecasts to 2033

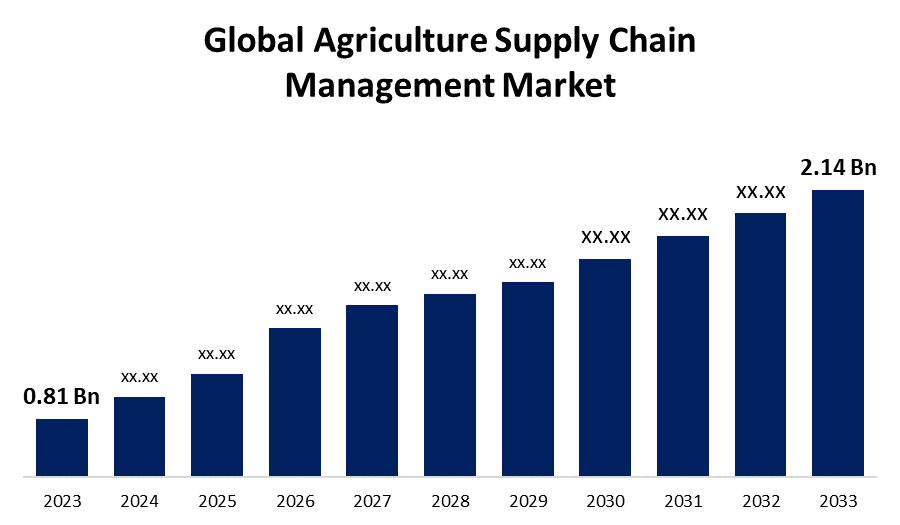

- The Global Agriculture Supply Chain Management Market Size was Valued at USD 0.81 Billion in 2023

- The Market Size is Growing at a CAGR of 10.20% from 2023 to 2033

- The Worldwide Agriculture Supply Chain Management Market Size is Expected to Reach USD 2.14 Billion by 2033

- North America is Expected to Grow the fastest during the forecast period.

Get more details on this report -

The Global Agriculture Supply Chain Management Market Size is Anticipated to Exceed USD 2.14 Billion by 2033, Growing at a CAGR of 10.20% from 2023 to 2033.

Market Overview

The procurement of raw materials, transforming them into finished products, and the delivery of those products to final consumers are the main activities that supply chains are focused on. In agribusiness, supply chain management, or SCM, refers to the management of the connections among the companies in charge of the productive production and delivery of products from the farm level to the end user, satisfying the latter's demands with consistency regarding quantity, quality, and cost. In actuality, this frequently refers to managing partnerships, both vertical and horizontal, as well as the interactions and procedures amongst businesses.

Globally, the market for supply chain management software is driven by the adoption of cloud-based software in agriculture. Compared to on-premises supply chain management software, cloud-based supply chain management software has several advantages. Companies use cloud SCM to save operating expenses and modernize their operations since it provides pay-per-use licenses and requires less IT setup. Additionally, cloud SCM providers are updating their offerings, which should further lower the cost of the solutions.

For instance, in April 2024, Bengaluru-based cloud solution company Eka Software was acquired by STG Quor specializes in CTRM capabilities within the metals ecosystem, whereas Eka offers supply chain solutions and commodities trade and risk management (CTRM) with a focus on the soft agriculture and energy sectors. The Quor Group, one of STG's portfolio companies, will be merged with Eka Software Solutions to offer a comprehensive software suite, according to the US-based equity firm's announcement. Quor specializes in CTRM capabilities within the metals ecosystem, while Bengaluru-based Eka offers supply chain solutions and commodities trade and risk management (CTRM) with a focus on the soft agriculture and energy sectors.

The demand for supply chain visibility and cloud-based supply chain management software, along with an increase in agribusiness businesses' need for demand management solutions, are some of the reasons driving the growth of the global agriculture supply chain management market.

Report Coverage

This research report categorizes the market for the global agriculture supply chain management market based on various segments and regions forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global agriculture supply chain management market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global agriculture supply chain management market.

Global Agriculture Supply Chain Management Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023 : | USD 0.81 Billion |

| Forecast Period: | 2023 – 2033 |

| Forecast Period CAGR 2023 – 2033 : | 10.20% |

| 023 – 2033 Value Projection: | USD 2.14 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 222 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Component, By Solution, By Deployment, By Region |

| Companies covered:: | FCE Group AG, Agri Value Chain, Bext360, Ambrosus, ChainPoint, AgriDigital, eHarvestHub, Eka, GrainChain, Geora Ltd., IBM, Trellis Ltd., Intellync, SAP SE, Others |

| Pitfalls & Challenges: | Covid-19 Impact, Challenge, Future,Growth and Analysis |

Get more details on this report -

Driving Factors

The market has expanded significantly as a result of rising agricultural product demand and cutting-edge methods. To increase their market share and geographic reach, businesses have partnered, invested, and introduced new products. In addition, the use of cloud-based software has been steadily increasing recently for a variety of agricultural supply chain and demand operations. A cloud-based supply chain benefits consumers in several ways. A significant reduction in the overall cost of solutions is achieved when several cloud vendors enhance their offerings. Agriculture-based enterprises benefit from a multitude of advantages, some of which are reduced risk, more visibility, quicker deployment, and increased flexibility.

Restraining Factors

The price of the finished products that are supplied is increased by the expense of using an agricultural supply chain management system. Small-scale businesses frequently lack the funding to handle the significantly higher costs of information processing and business-to-business transaction management. The delivery process is hampered by the period required for software installation and deployment, which leaves the recipient uncertain. Agriculture products' ultimate pricing is negatively impacted by longer processing times, which also raise overhead expenses.

Market Segmentation

The global agriculture supply chain management market share is segmented into component, solution, and deployment.

- The hardware segment dominates the market with the largest market share through the forecast period.

Based on the component, the global agriculture supply chain management market is segmented into hardware, solutions, and services. Among these, the hardware segment dominates the market with the largest market share through the forecast period. The growing demand for cutting-edge hardware and technology is likely to propel this segment's performance during the forecast period. To boost supply capacity, major manufacturers and market participants require a variety of cutting-edge components. The size of this market has increased significantly due to the rising demand for cutting-edge machinery and technology.

- The manufacturing execution system segment is anticipated to grow at the fastest CAGR growth through the forecast period.

Based on the solution, the global agriculture supply chain management market is segmented into manufacturing execution system, procurement & sourcing, transportation management system, supply chain planning, and warehouse management system. Among these, the manufacturing execution system segment is anticipated to grow at the fastest CAGR growth through the forecast period. Due to people's growing need for agricultural products and their increasing need for sophisticated agricultural equipment. The main prerequisite for satisfying the supply chain, and demand, and giving customers the necessary items is transportation. Transportation facility management enables manufacturers to finish deliveries on schedule.

- The on-premise segment accounted for the largest revenue share through the forecast period.

Based on the deployment, the global agriculture supply chain management market is segmented into on-demand & cloud-based, and on-premise. Among these, the on-premise segment accounted for the largest revenue share through the forecast period. On-premise services help customers in real-time at their locations, which will support the expansion of the market. One of the main drivers of growth has been the organization of important data and the analysis of that data for the customer through phone conversations and emails. Throughout the process, the data can be collected and shown using the on-premises model's capabilities. It is anticipated that the form will make use of chatbots to leverage its information technology infrastructure.

Regional Segment Analysis of the Global Agriculture Supply Chain Management Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the global agriculture supply chain management market over the predicted timeframe.

Get more details on this report -

Asia Pacific is anticipated to hold the largest share of the global agriculture supply chain management market over the predicted timeframe. Its dominant position in the agriculture supply chain management market is a result of its significant global contribution. The creation of several new companies and firms making significant investments in agriculture is what is responsible for the robust expansion of the Asia Pacific economy. Due to the growing need for contemporary technology and equipment, productivity is predicted to rise quickly.

North America is expected to grow at the fastest CAGR growth of the global agriculture supply chain management market during the forecast period. Online solutions are being used more and more by the agricultural supply chain service sector in North America, especially in the United States, to increase productivity and streamline processes. Agricultural producers can trace their supply chains and suppliers more easily owing to online technologies that automate the offline manual processes of supply chain services. To improve coordination and decision-making, digital platforms are also being used for data exchange and collaboration amongst different supply chain actors.

In addition, there are government initiatives such as the USDA's Farm Service Agency's grant program. Among the federal departments, USDA is distinct due to the scope of its Mission Areas and its ability to reach out to urban, rural, and tribal people all over the country. To remain competitive and sustainable in the next decades, American farmers, ranchers, forest owners, and other stakeholders must take action to lessen their susceptibility to climate change and improve their capacity for adaptation. USDA will make these industries and communities more resilient to climate change via planning for adaptation to it.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global agriculture supply chain management market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- FCE Group AG

- Agri Value Chain

- Bext360

- Ambrosus

- ChainPoint

- AgriDigital

- eHarvestHub

- Eka

- GrainChain

- Geora Ltd.

- IBM

- Trellis Ltd.

- Intellync

- SAP SE

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In May 2022, Intellync, a supplier of supply chain management systems, and Star Index formed a cooperation. The goal of the combined knowledge of the two businesses is to maximize benefits to the prospective customers through the reduction of resource requirements, improvement facilitation, data reporting, data capture, and risk assessment across the various supply chains associated with the food and agricultural industries.

- In November 2021, The world's largest business sustainability effort, the United Nations Global Compact (UNGC), now includes Eka Software Solutions as an official signatory. As a signatory, Eka incorporates the UNGC's tenets into its corporate processes to further advance sustainability for all parties involved, including partners, suppliers, consumers, and workers.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. Spherical Insights has segmented the global agriculture supply chain management market based on the below-mentioned segments:

Global Agriculture Supply Chain Management Market, By Component

- Hardware

- Solutions

- Services

Global Agriculture Supply Chain Management Market, By Solution

- Manufacturing Execution System

- Procurement & Sourcing

- Transportation Management System

- Supply Chain Planning

- Warehouse Management System

Global Agriculture Supply Chain Management Market, By Deployment

- On-Demand & Cloud-Based

- On-Premise

Global Agriculture Supply Chain Management Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. Which are the key companies that are currently operating within the market?FCE Group AG, Agri Value Chain, Bext360, Ambrosus, ChainPoint, AgriDigital, eHarvestHub, Eka, GrainChain, Inc., Geora Ltd., IBM, Trellis Ltd., Intellync, SAP SE, and Others.

-

2. What is the size of the global agriculture supply chain management market?The Global Agriculture Supply Chain Management Market Size is Expected to Grow from USD 0.81 Billion in 2023 to USD 2.14 Billion by 2033, at a CAGR of 10.20% during the forecast period 2023-2033.

-

3. Which region is holding the largest share of the market?Asia Pacific is anticipated to hold the largest share of the global agriculture supply chain management market.

Need help to buy this report?