Global Automotive Camera Market Size, Share, and COVID-19 Impact Analysis, By Type (Stereo and Monocular), By Application Type (Park Assist System, Lane Departure Warning System, Blind Spot Detection, Lane Keep Assist, Road Sign Assistance, Adaptive Cruise Control (ACC), Intelligent Headlight Control, and Others), By Technology Type (Digital Camera, Infrared Camera, and Thermal Camera), By Vehicle Type (Passenger Cars and Commercial Vehicles), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033

Industry: Automotive & TransportationGlobal Automotive Camera Market Insights Forecasts to 2033

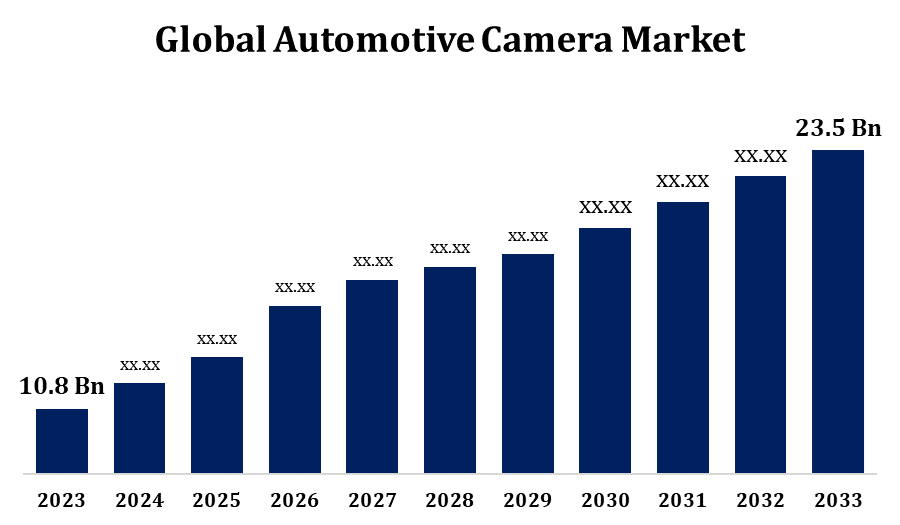

- The Automotive Camera Market Size Was Valued at USD 10.8 Billion in 2023.

- The Market Size is Growing at a CAGR of 8.08% from 2023 to 2033.

- The Global Automotive Camera Market Size is Expected to reach USD 23.5 Billion By 2033.

- Asia Pacific is Expected to Grow the fastest during the Forecast period.

Get more details on this report -

The Global Automotive Camera Market Size is Expected to reach USD 23.5 Billion by 2033, at a CAGR of 8.08% during the Forecast period 2023 to 2033.

The Automotive Camera Market is experiencing rapid growth, driven by increasing demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies. These cameras enhance vehicle safety by enabling features like lane departure warning, adaptive cruise control, and collision avoidance. Rising government regulations on vehicle safety and the growing adoption of electric vehicles further boost market expansion. Key players are investing in high-resolution cameras, night vision, and AI-powered imaging for improved performance. The market is segmented by technology (thermal, infrared, digital), vehicle type (passenger, commercial), and application (ADAS, parking assistance, blind-spot detection). Asia-Pacific leads due to high vehicle production, followed by North America and Europe. With continuous innovations and integration of AI, the automotive camera market is poised for substantial growth in the coming years.

Automotive Camera Market Value Chain Analysis

The automotive camera market value chain involves multiple stages, from raw material suppliers to end users. It begins with component manufacturers providing essential parts like lenses, image sensors, and processors. These components are then assembled by camera module manufacturers, who integrate features such as AI-based image processing and thermal imaging. Tier-1 suppliers collaborate with automakers to embed cameras into advanced driver-assistance systems (ADAS) and autonomous vehicles. Original Equipment Manufacturers (OEMs) incorporate these systems into vehicles, ensuring compliance with safety regulations. Distribution channels include direct sales, aftermarket suppliers, and retailers. Software developers play a crucial role in enhancing camera functionality with AI, computer vision, and data analytics. The increasing demand for smart vehicles and safety regulations continues to drive innovation and expansion in this market.

Automotive Camera Market Opportunity Analysis

The automotive camera market presents significant growth opportunities driven by advancements in autonomous driving, increasing ADAS adoption, and stringent safety regulations. The rising demand for electric and connected vehicles further accelerates market expansion. Innovations in AI-powered imaging, 360-degree surround-view cameras, and thermal vision create new revenue streams. Emerging markets in Asia-Pacific and Latin America offer lucrative opportunities due to growing vehicle production and safety awareness. The aftermarket segment is also expanding, with consumers upgrading vehicles for enhanced safety features. Additionally, partnerships between automakers, tech companies, and sensor manufacturers fuel innovation. The integration of automotive cameras with LiDAR and radar for Level 3+ autonomous driving opens new possibilities. As smart mobility gains traction, the automotive camera market is poised for substantial long-term growth.

Global Automotive Camera Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 10.8 Billion |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | 8.08% |

| 2033 Value Projection: | USD 23.5 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 240 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Type, By Application Type, By Technology Type, By Vehicle Type, By Region and COVID-19 Impact Analysis |

| Companies covered:: | Bosch, Mobileye, Continental, Sharp, Renesas Electronics, LG Innotek, STMicroelectronics, Texas Instruments, Cypress Semiconductor, Aptiv, Omnivision Technologies, Valeo, Nvidia, Sony and others key players. |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Market Dynamics

Automotive Camera Market Dynamics

Increasing adoption of 360-degree cameras is driving market growth

The increasing adoption of 360-degree cameras is a key driver of growth in the automotive camera market. These cameras provide a comprehensive view of a vehicle’s surroundings, enhancing safety and convenience for drivers. They are widely integrated into advanced driver-assistance systems (ADAS) for applications such as parking assistance, blind-spot monitoring, and collision avoidance. Automakers are prioritizing 360-degree camera systems to meet stringent safety regulations and improve user experience. The growing demand for autonomous and connected vehicles further accelerates their adoption. Additionally, advancements in AI-powered image processing and high-resolution imaging enhance the functionality of these cameras. With rising consumer awareness and the push for improved road safety, the adoption of 360-degree cameras will continue to expand, significantly contributing to the automotive camera market’s growth.

Restraints & Challenges

High production and integration costs hinder widespread adoption, particularly in budget and mid-range vehicles. Technical limitations, such as poor performance in extreme weather or low-light conditions, affect reliability. Data security and privacy concerns also pose risks, as connected vehicle cameras collect and transmit sensitive information. Additionally, regulatory variations across regions create compliance challenges for manufacturers. The complexity of integrating cameras with other sensors, such as LiDAR and radar, adds to development costs and time. The automotive semiconductor shortage further impacts supply chains, delaying production. Moreover, consumer resistance to fully autonomous technology slows adoption rates.

Regional Forecasts

North America Market Statistics

Get more details on this report -

North America is anticipated to dominate the Automotive Camera Market from 2023 to 2033. Strict government regulations, such as the National Highway Traffic Safety Administration (NHTSA) mandates on rearview cameras, drive adoption. The region’s strong presence of key automakers and technology companies fosters innovation in AI-powered imaging, thermal vision, and 360-degree camera systems. Rising consumer preference for high-end safety features in passenger vehicles further boosts market growth. Additionally, the growing electric vehicle (EV) market and the push for Level 3+ autonomous vehicles contribute to increased camera integration.

Asia Pacific Market Statistics

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. China, Japan, South Korea, and India are leading the market due to strong automotive manufacturing hubs and government mandates for vehicle safety. The rapid expansion of electric vehicles (EVs) and autonomous driving technologies further boosts demand for high-resolution and AI-powered cameras. Growing urbanization and rising disposable income have increased consumer demand for safety and convenience features in vehicles. With continuous technological advancements and increasing investments in smart mobility, the Asia-Pacific region is expected to dominate the global automotive camera market in the coming years.

Segmentation Analysis

Insights by Application Type

The park assist system segment accounted for the largest market share over the forecast period 2023 to 2033. Advanced parking systems use multiple cameras, including 360-degree and rearview cameras, to provide real-time visuals and automated guidance. Rising urbanization and crowded parking spaces have heightened the need for efficient parking solutions, further driving adoption. Automakers are integrating AI-powered image processing and ultrasonic sensors to enhance accuracy and automation. Stringent safety regulations mandating rearview cameras in vehicles also contribute to market expansion. Additionally, the growing penetration of electric and autonomous vehicles accelerates the demand for advanced parking technologies. As consumers seek smarter and safer driving experiences, the park assist system segment is expected to continue its upward growth trajectory in the automotive camera market.

Insights by Type

The stereo segment accounted for the largest market share over the forecast period 2023 to 2033. Stereo cameras use dual-lens technology to accurately measure distances, making them essential for advanced driver-assistance systems (ADAS) such as automatic emergency braking, lane-keeping assistance, and pedestrian detection. Automakers are increasingly adopting stereo cameras to enhance vehicle safety and meet stringent regulations. The growing demand for autonomous and semi-autonomous vehicles further accelerates this segment’s expansion, as stereo cameras improve object detection and environmental mapping. Additionally, advancements in AI-driven image processing enhance their performance in low-light and adverse weather conditions. With the increasing integration of stereo cameras in both passenger and commercial vehicles, this segment is poised for continuous growth in the automotive camera market.

Insights by Technology Type

The digital segment accounted for the largest market share over the forecast period 2023 to 2033. The growth is due to its high-resolution imaging, real-time processing, and seamless integration with advanced driver-assistance systems (ADAS). Unlike analog cameras, digital cameras offer superior image clarity, enhancing functions like lane departure warning, blind-spot detection, and adaptive cruise control. Automakers are increasingly adopting digital cameras to improve vehicle safety and meet evolving regulatory standards. The shift toward electric and autonomous vehicles further accelerates demand, as digital cameras play a crucial role in sensor fusion with LiDAR and radar systems. Additionally, advancements in AI-powered image processing and night vision capabilities enhance their effectiveness in various driving conditions.

Insights by Vehicle Type

The passenger cars segment accounted for the largest market share over the forecast period 2023 to 2033. Automakers are integrating cameras for applications such as adaptive cruise control, lane departure warning, blind-spot detection, and park assist to enhance vehicle safety and convenience. Stringent government regulations mandating rearview cameras and ADAS adoption further accelerate market expansion. Additionally, the rising popularity of electric and autonomous vehicles boosts the need for high-resolution and AI-powered cameras. Consumers are increasingly prioritizing safety and automation, leading to a surge in demand for camera-based systems in mid-range and luxury passenger vehicles. With continuous technological advancements and regulatory support, the passenger cars segment is expected to drive significant growth in the automotive camera market.

Recent Market Developments

- In February 2024, VIA Optronics AG has entered into a design and development agreement with Immervision Inc. to create VIA’s next-generation automotive camera.

Competitive Landscape

Major players in the market

- Bosch

- Mobileye

- Continental

- Sharp

- Renesas Electronics

- LG Innotek

- STMicroelectronics

- Texas Instruments

- Cypress Semiconductor

- Aptiv

- Omnivision Technologies

- Valeo

- Nvidia

- Sony

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Automotive Camera Market, Type Analysis

- Stereo

- Monocular

Automotive Camera Market, Application Type Analysis

- Park Assist System

- Lane Departure Warning System

- Blind Spot Detection

- Lane Keep Assist

- Road Sign Assistance

- Adaptive Cruise Control (ACC)

- Intelligent Headlight Control

- Others

Automotive Camera Market, Technology Type Analysis

- Digital Camera

- Infrared Camera

- Thermal Camera

Automotive Camera Market, Vehicle Type Analysis

- Passenger Cars

- Commercial Vehicles

Automotive Camera Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the market size of the Automotive Camera Market?The global Automotive Camera Market is expected to grow from USD 10.8 billion in 2023 to USD 23.5 billion by 2033, at a CAGR of 8.08% during the forecast period 2023-2033.

-

2. Who are the key market players of the Automotive Camera Market?Some of the key market players of the market are Bosch, Mobileye, Continental, Sharp, Renesas Electronics, LG Innotek, STMicroelectronics, Texas Instruments, Cypress Semiconductor, Aptiv, Omnivision Technologies, Valeo, Nvidia, Sony.

-

3. Which segment holds the largest market share?The passenger cars segment holds the largest market share and is going to continue its dominance.

Need help to buy this report?