Global Digital Battlefield Market Size, Share, and COVID-19 Impact Analysis, By Technological Innovation (Artificial Intelligence, Cyber Warfare Solutions, Simulation Training Tools, Autonomous Systems), By Application Sector (Military Operations, Defense Research, Training and Simulation, Strategic Planning), By Deployment Model (On-Premises, Cloud-Based, Hybrid Solutions), By User Type (Government Defense Agencies, Private Defense Contractors, Military Personnel), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033

Industry: Aerospace & DefenseGlobal Digital Battlefield Market Size Insights Forecasts to 2033

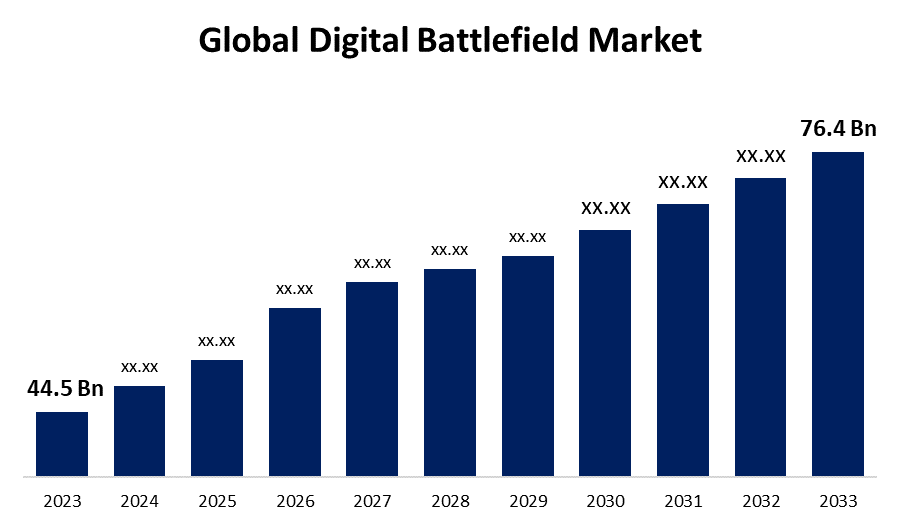

- The Digital Battlefield Market Size was valued at USD 44.5 Billion in 2023.

- The Market Size is growing at a CAGR of 5.55% from 2023 to 2033.

- The Worldwide Digital Battlefield Market is expected to reach USD 76.4 Billion by 2033.

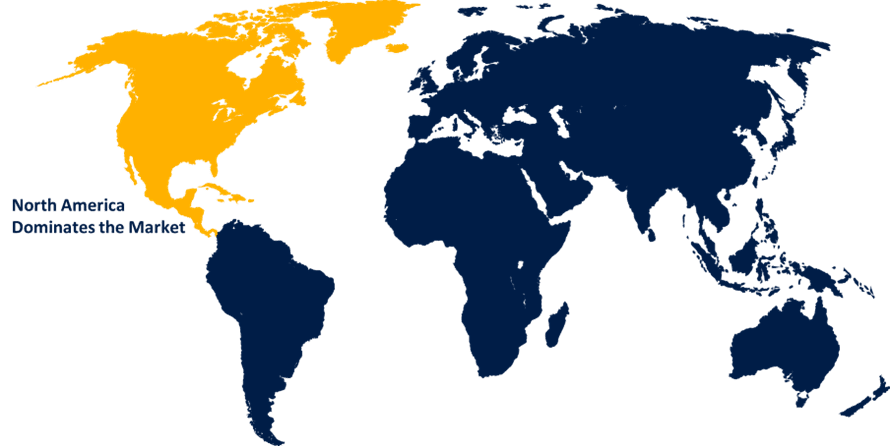

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

The Global Digital Battlefield Market Size is expected to reach USD 76.4 Billion by 2033, at a CAGR of 5.55% during the forecast period 2023 to 2033.

The digital battlefield market is rapidly evolving as modern warfare integrates advanced technologies like AI, IoT, cloud computing, and big data analytics. Militaries worldwide are investing in real-time intelligence, cybersecurity, and autonomous systems to enhance situational awareness and combat efficiency. Key components include digital command and control (C2), electronic warfare, and network-centric operations. Growing geopolitical tensions and the need for seamless communication among defense forces are driving market expansion. North America leads due to significant defense budgets, while Asia-Pacific shows high growth potential. Challenges include cybersecurity threats and integration complexities. Leading players such as Lockheed Martin, Raytheon, and BAE Systems are innovating in secure communication and AI-driven battlefield management. The future of warfare is increasingly digital, with smart and interconnected defense ecosystems shaping modern combat strategies.

Digital Battlefield Market Value Chain Analysis

The digital battlefield market value chain comprises multiple interconnected segments, starting with technology providers that develop AI, IoT, cybersecurity, and cloud solutions. These innovations are integrated into defense contractors like Lockheed Martin and Raytheon, which design battlefield systems, including command and control (C2), surveillance, and electronic warfare tools. System integrators play a crucial role in combining various digital solutions into a seamless operational framework for defense forces. Governments and defense agencies act as primary buyers, driving demand through military modernization programs. End-users, including army, navy, and air forces, deploy these systems for real-time intelligence and combat efficiency. Supporting elements such as RandD firms, regulatory bodies, and cybersecurity firms ensure compliance, security, and innovation, making the digital battlefield ecosystem more resilient and effective.

Digital Battlefield Market Opportunity Analysis

The digital battlefield market presents significant growth opportunities driven by increasing defense budgets, rising geopolitical tensions, and rapid technological advancements. The adoption of AI, IoT, and cloud computing in military operations is transforming combat strategies, enhancing real-time decision-making, and improving operational efficiency. The demand for cybersecurity solutions is growing as digital warfare increases the risk of cyber threats. Emerging economies in Asia-Pacific and the Middle East are heavily investing in modernizing their defense infrastructure, creating new market prospects. Additionally, the integration of unmanned systems, autonomous weapons, and 5G communication networks offers expansion opportunities for defense contractors and technology firms. Collaboration between governments and private sector players in developing smart and connected battlefield solutions further strengthens the market, making it a key focus for future defense innovation.

Global Digital Battlefield Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 44.5 Billion |

| Forecast Period: | 2023 – 2033 |

| Forecast Period CAGR 2023 – 2033 : | 5.55% |

| 023 – 2033 Value Projection: | USD 76.4 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 214 |

| Tables, Charts & Figures: | 104 |

| Segments covered: | By Technological Innovation, By Application Sector, By Application Sector, By User Type, By Region |

| Companies covered:: | Microsoft Raytheon Technologies Palantir Technologies Thales Group Hewlett Packard Enterprise Northrop Grumman BAE Systems Cisco Systems IBM General Dynamics L3Harris Technologies Oracle Leonardo Lockheed Martin Boeing and Others |

| Pitfalls & Challenges: | COVID-19 Empact,Challenges, Future, Growth, & Analysis |

Get more details on this report -

Market Dynamics

Digital Battlefield Market Dynamics

Growing Need for Cutting-Edge Technology Integration

The digital battlefield market is experiencing significant growth due to the increasing need for cutting-edge technology integration. Advanced systems such as AI, IoT, big data analytics, and 5G communication are enhancing military operations by improving situational awareness, decision-making, and combat effectiveness. Defense forces worldwide are investing in cloud-based command and control (C2) systems, cybersecurity solutions, and autonomous platforms to gain a strategic edge. The rise of network-centric warfare and electronic warfare capabilities further drives demand for seamless, real-time data exchange. Additionally, emerging economies are modernizing their defense infrastructure, boosting market expansion. Companies are focusing on RandD to develop smart, connected battlefield solutions, ensuring operational efficiency and security. As digital transformation accelerates, technology-driven warfare will define the future of military engagements globally.

Restraints and Challenges

One major concern is cybersecurity threats, as increased digitalization makes military networks vulnerable to cyberattacks and data breaches. Integration complexities also pose challenges, as defense forces must seamlessly combine diverse technologies like AI, IoT, and cloud computing across various platforms. High implementation costs and budget constraints in some regions can slow adoption. Additionally, interoperability issues arise when integrating new digital solutions with legacy defense systems. Regulatory and compliance challenges, including data privacy laws and international defense policies, further complicate market expansion. The dependence on advanced technologies also raises risks of system failures and potential reliance on a few key suppliers. Overcoming these challenges requires robust security frameworks, strategic partnerships, and continuous innovation in defense technology.

Regional Forecasts

North America Market Statistics

Get more details on this report -

North America is anticipated to dominate the Digital Battlefield Market from 2023 to 2033. The U.S. Department of Defense is heavily investing in AI-driven warfare, cybersecurity solutions, and next-generation communication systems to enhance battlefield efficiency. The region is also at the forefront of network-centric warfare, integrating IoT, cloud computing, and big data analytics for real-time decision-making. Growing concerns over cyber warfare and geopolitical tensions are driving further investments in digital command and control (C2) systems, electronic warfare, and unmanned platforms. Additionally, collaborations between defense agencies and private tech firms are accelerating innovation, ensuring North America maintains its leadership in the evolving digital battlefield landscape.

Asia Pacific Market Statistics

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. China, India, Japan, and South Korea are heavily investing in AI-driven warfare, cybersecurity, and advanced communication systems to strengthen their defense capabilities. The adoption of network-centric warfare, electronic warfare, and autonomous military platforms is increasing, driven by regional security concerns and territorial disputes. Governments are collaborating with domestic and global defense technology firms to enhance real-time intelligence, surveillance, and battlefield management systems. Additionally, advancements in 5G, IoT, and cloud computing are further transforming digital warfare strategies. With ongoing defense upgrades and growing demand for high-tech military solutions, Asia-Pacific is emerging as a key player in the global digital battlefield market.

Segmentation Analysis

Insights by Technological Innovation

The Artificial Intelligence segment accounted for the largest market share over the forecast period 2023 to 2033. AI-powered systems improve situational awareness, threat detection, and predictive analytics, enabling faster and more accurate responses in combat scenarios. Autonomous weapons, unmanned aerial vehicles (UAVs), and AI-driven surveillance systems are being rapidly adopted to reduce human risk and increase operational efficiency. AI also plays a crucial role in cybersecurity, protecting military networks from cyber threats and data breaches. Governments and defense organizations are heavily investing in AI research and development to strengthen their digital warfare capabilities. As AI technology advances, its integration into military operations will continue to reshape modern battlefield strategies worldwide.

Insights by Application Sector

The Defense Research segment accounted for the largest market share over the forecast period 2023 to 2033. Research institutions are focused on advancing AI, machine learning, autonomous systems, and cybersecurity solutions to improve battlefield effectiveness. Ongoing RandD efforts aim to create smarter command and control systems, innovative communication networks, and advanced defense platforms such as drones and robotic systems. Collaboration between public defense bodies and private tech firms accelerates the development of next-gen digital warfare technologies. Furthermore, defense research helps address integration challenges, ensuring seamless operation across various platforms. As global defense priorities shift toward modernization and digital transformation, the defense research segment will continue to play a vital role in shaping the future of military operations and strategic defense systems.

Insights by Deployment Model

The On-Premises segment accounted for the largest market share over the forecast period 2023 to 2033. On-premises solutions offer the advantage of maintaining sensitive military data within secure, isolated environments, reducing the risk of cyber threats and external breaches. These systems support critical applications such as command and control, surveillance, and real-time data processing, all of which are essential in military operations. Many defense forces prefer on-premises infrastructure for its reliability, scalability, and direct control over system performance. As the demand for secure, high-performance digital battlefield platforms increases, defense agencies are investing in on-premises solutions to ensure seamless integration with legacy systems while maintaining operational integrity. The need for advanced, localized systems in high-stakes environments continues to fuel growth in the on-premises segment.

Insights by User Type

The government agencies segment accounted for the largest market share over the forecast period 2023 to 2033. Governments worldwide are prioritizing the development and deployment of AI, IoT, cybersecurity, and cloud-based systems to enhance national defense capabilities and operational efficiency. As defense agencies move toward more network-centric and data-driven warfare, there is a growing demand for real-time intelligence, autonomous systems, and secure communication platforms. Additionally, governments are collaborating with defense contractors and technology firms to ensure seamless integration of cutting-edge digital solutions into their military infrastructure. Geopolitical instability and evolving security threats further accelerate investments in digital warfare strategies. As defense budgets rise, government agencies continue to drive innovation and growth in the digital battlefield market, shaping the future of military operations globally.

Recent Market Developments

- In May 2024, L3Harris Technologies enhanced the U.S. Army's capabilities with its new Hawkeye III Lite Very Small Aperture Terminal (VSAT), providing reliable and scalable SATCOM solutions.

Competitive Landscape

Major players in the market

- Microsoft

- Raytheon Technologies

- Palantir Technologies

- Thales Group

- Hewlett Packard Enterprise

- Northrop Grumman

- BAE Systems

- Cisco Systems

- IBM

- General Dynamics

- L3Harris Technologies

- Oracle

- Leonardo

- Lockheed Martin

- Boeing

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Digital Battlefield Market, Technological Innovation Analysis

- Artificial Intelligence

- Cyber Warfare Solutions

- Simulation Training Tools

- Autonomous Systems

Digital Battlefield Market, Application Sector Analysis

- Military Operations

- Defense Research

- Training and Simulation

- Strategic Planning

Digital Battlefield Market, Deployment Sector Analysis

- On-Premises

- Cloud-Based

- Hybrid Solutions

Digital Battlefield Market, User Type Analysis

- Government Defense Agencies

- Private Defense Contractors

- Military Personnel

Digital Battlefield Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East and Africa

Frequently Asked Questions (FAQ)

-

1. What is the market size of the Digital Battlefield Market?The global Digital Battlefield Market is expected to grow from USD 44.5 billion in 2023 to USD 76.4 billion by 2033, at a CAGR of 5.55% during the forecast period 2023-2033.

-

2. Who are the key market players of the Digital Battlefield Market?Some of the key market players of the market are Microsoft, Raytheon Technologies, Palantir Technologies, Thales Group, Hewlett Packard Enterprise, Northrop Grumman, BAE Systems, Cisco Systems, IBM, General Dynamics, L3Harris Technologies, Oracle, Leonardo, Lockheed Martin, Boeing.

-

3. Which segment holds the largest market share?The government agencies segment holds the largest market share and is going to continue its dominance.

Need help to buy this report?