Global Healthcare Integration Market Size, Share, and COVID-19 Impact Analysis, By Product (Interface/Integration Engines, Medical Device Integration Software, Media Integration Solutions, and Other Integration Tools), By End-Use (Hospitals, Diagnostic Centers, Laboratories, Clinics, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033

Industry: HealthcareGlobal Healthcare Integration Market Insights Forecasts to 2033

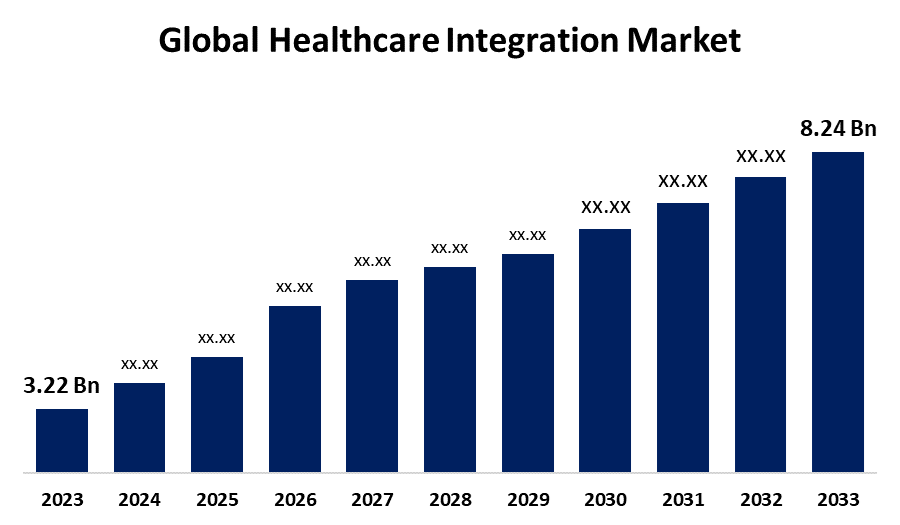

- The Global Healthcare Integration Market Size was Valued at USD 3.22 Billion in 2023

- The Market Size is Growing at a CAGR of 9.85% from 2023 to 2033

- The Worldwide Healthcare Integration Market Size is Expected to Reach USD 8.24 Billion by 2033

- Asia Pacific is Expected to Grow the fastest during the forecast period.

Get more details on this report -

The Healthcare Integration Market Size is Anticipated to Exceed USD 8.24 Billion by 2033, Growing at a CAGR of 9.85% from 2023 to 2033.

Market Overview

Healthcare integration involves the blend and harmonization of different healthcare services, systems, and technologies that bring forth continuous, efficient, and patient-centered involvement. As chronic disease cases rise, the aging populations increase, and the intricacy of care needs advance, healthcare providers are deploying integration solutions to improve operational efficiency, patient outcomes, and cost-cutting in the process. The widespread acceptance of EHRs, telemedicine platforms, and HIEs underlies the critical role of integration technologies. These technologies enable data sharing securely, real-time insights into the system, and even automated workflows that make the delivery of healthcare more efficient and patient-centric. There are government initiatives to promote interoperability and regulations such as the HITECH Act in the United States, which accelerates market growth. Therefore, even though these exist, the Asian-Pacific regions are opening up more opportunities and are in higher demand to expand health infrastructure and growing digital penetration. The market is highly competitive, with key players focusing on innovation, strategic partnerships, and mergers to capture market share and address evolving healthcare demands.

Report Coverage

This research report categorizes the market for healthcare integration market based on various segments and regions forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the healthcare integration market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the healthcare integration market.

Global Healthcare Integration Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023 : | 3.22 Billion |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | CAGR of 9.85% |

| 2033 Value Projection: | 8.24 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 220 |

| Tables, Charts & Figures: | 111 |

| Segments covered: | By Product, By End-Use, and By Region |

| Companies covered:: | Corepoint Health, IBM, Oracle Corporation, Epic Systems Corporation, Summit Healthcare Services, Inc., Orion Health, Interfaceware, Allscripts Healthcare Solutions, Inc., Intersystems Corporation, Quality Systems, Inc., Cerner Corporation, Infor, Inc., Optum Inc., Cognizant, Change Healthcare, Others, |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The market is primarily driven by the growing requirement for seamless data exchange and interoperability among healthcare systems; with health providers increasingly seeking more efficient ways of managing patient information across different platforms. Widespread adoption of EHRs and HIEs also gives a boost to the requirement of integration technologies. Technological advancements such as artificial intelligence (AI), machine learning (ML), and cloud computing interpretive changed the healthcare integration landscape. Such technology is real-time for analyzing data, simplifies the workflow process, and takes good care of the patients. Moreover, increased rates of chronic diseases and age groups increase care needs through the model of coordination care.

Restraining Factors

The high implementation and maintenance costs of integration solutions, interoperability challenges among diverse healthcare systems, and also strict data privacy regulations restrict the growth of the market. Less number of skilled IT professionals and resistance by health service organizations toward adopting the latest technologies is one of the major restraints for extensive adoption of integration solutions.

Market Segmentation

The healthcare integration market share is classified into product type and end-use.

- The medical device integration software segment is expected to hold the largest share through the forecast period.

Based on the product type, the healthcare integration market is categorized into interface/integration engines, medical device integration software, media integration solutions, and other integration tools. Among these, the medical device integration software segment is expected to hold the largest share through the forecast period. This is because of the system that gathers the dynamic sign statistics of the patient from all the health monitoring devices and puts them together with the electronic medical record system. The whole data transfer erases the need for manual data input and transfer thereby, enlightening efficiency, accuracy, efficiency, and fewer errors.

- The hospitals segment is expected to hold the largest share through the forecast period.

Based on the end-use, the healthcare integration market is categorized as hospitals, diagnostic centers, laboratories, clinics, and others. Among these, the hospitals segment is expected to hold the largest share through the forecast period. This is because there is a growing demand to minimize errors, increase efficiency, decrease the cost of health care, and enhance patient safety. Furthermore, the integration of health systems to handle the large quantities of data that the different departments of the hospital collect as a result of the increase in communicable and non-communicable diseases contributes to an increase in the number of patients seeking consultation, treatment, and therapy in hospitals.

Regional Segment Analysis of the Healthcare Integration Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the healthcare integration market over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the largest share of the healthcare integration market over the forecast period. This is owing to the presence of highly established healthcare infrastructure, the high importance of patient fulfillment, the growing patient population, and massive healthcare disbursement in the region. North American governments have issued regulatory mandates and offered financial incentives that have allowed healthcare providers to adopt IT solutions, which in turn has fueled the healthcare data integration process. North America's healthcare industry is embracing a shift toward value-based care, a model focused on enhancing patient outcomes and cost reduction.

Asia Pacific is expected to grow at the fastest CAGR growth in the healthcare integration market during the forecast period. The region's large and growing population, with an increasing incidence of chronic diseases, is driving the demand for healthcare data integration solutions. These solutions are focused on improving patient care and cost reduction. Additionally, key players in the APAC region are strategically expanding their product portfolios, making significant investments, and forming strategic partnerships. This strategic approach caters to the increasing demand for healthcare data integration solutions that offer affordability and user-friendliness, ensuring accessibility and robust functionality.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the healthcare integration market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Corepoint Health

- IBM

- Oracle Corporation

- Epic Systems Corporation

- Summit Healthcare Services, Inc.

- Orion Health

- Interfaceware

- Allscripts Healthcare Solutions, Inc.

- Intersystems Corporation

- Quality Systems, Inc.

- Cerner Corporation

- Infor, Inc.

- Optum Inc.

- Cognizant

- Change Healthcare

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In January 2023, CipherHealth Inc., a patient engagement technology company, partnered with SADA, Inc., a leading business and technology consultancy, to integrate social determinants of health (SDOH) data integration into patient care. This collaboration aims to make the integration of SDOH data more accessible and actionable for healthcare providers and contribute to a healthcare system that is equitable and effective in its approach.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. Spherical Insights has segmented the healthcare integration market based on the below-mentioned segments:

Global Healthcare Integration Market, By Product Type

- Interface/Integration Engines

- Medical Device Integration Software

- Media Integration Solutions

- Other Integration Tools

Global Healthcare Integration Market, By End-Use

- Hospitals

- Diagnostic Centers

- Laboratories

- Clinics

- Others

Global Healthcare Integration Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the CAGR of the global healthcare integration market?The global healthcare integration market is projected to expand at 9.85% during the forecast period.

-

2. Who are the top key players in the global healthcare integration market?The key players in the global healthcare integration market are Corepoint Health, IBM, Oracle Corporation, Epic Systems Corporation, Summit Healthcare Services, Inc., Orion Health, Interfaceware, Allscripts Healthcare Solutions, Inc., InterSystems Corporation, Quality Systems, Inc., Cerner Corporation, Infor, Inc., Optum Inc., Cognizant, Change Healthcare, and others.

-

3. Which region holds the largest share of the healthcare integration market?North America is anticipated to hold the largest share of the healthcare integration market over the predicted timeframe.

Need help to buy this report?