Global Military Vehicle Sustainment Market Size, Share, and COVID-19 Impact Analysis, by Vehicle Type (Armored Vehicles, Military Trucks), by End User (Army, Navy, Air Force), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033

Industry: Aerospace & DefenseGlobal Military Vehicle Sustainment Market Insights Forecasts to 2033

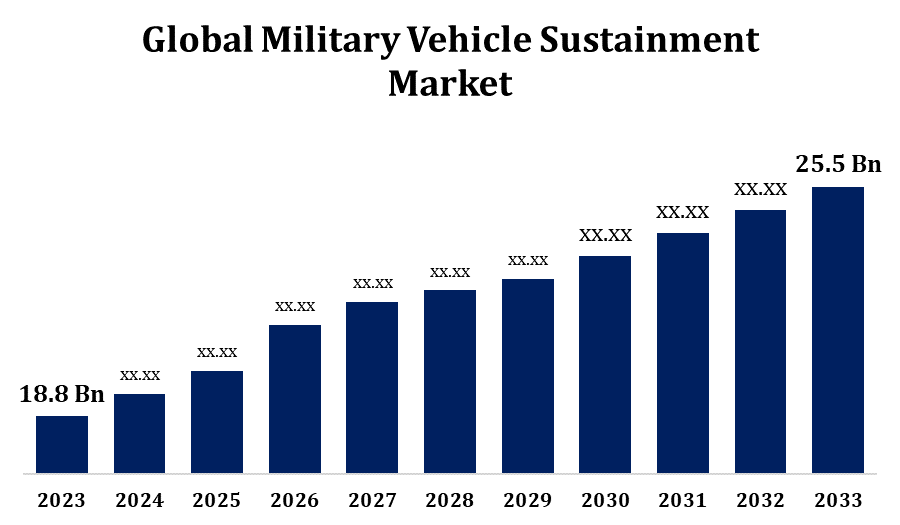

- The Military Vehicle Sustainment Market was valued at USD 18.8 Billion in 2023.

- The Market is growing at a CAGR of 3.10% from 2023 to 2033.

- The Worldwide Military Vehicle Sustainment Market is expected to reach USD 25.5 Billion by 2033.

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

The Global Military Vehicle Sustainment Market is expected to reach USD 25.5 Billion by 2033, at a CAGR of 3.10% during the forecast period 2023 to 2033.

The military vehicle sustainment market focuses on the maintenance, repair, overhaul (MRO), and lifecycle management of military vehicles, ensuring their readiness and operational efficiency. This market is driven by increasing defense budgets, technological advancements, and the growing need to extend the service life of existing fleets. Key components include supply chain management, predictive maintenance, and modernization programs to enhance vehicle performance and adaptability. Demand for specialized services, such as condition-based maintenance and retrofitting, is rising as militaries prioritize cost-effectiveness and sustainability. Regional dynamics, influenced by geopolitical tensions and modernization initiatives, play a significant role in market growth. Partnerships between defense contractors and governments further fuel innovation. As military operations grow more complex, sustaining vehicles efficiently remains a strategic priority worldwide.

Military Vehicle Sustainment Market Value Chain Analysis

The military vehicle sustainment market value chain encompasses a series of interconnected processes ensuring vehicle reliability and operational readiness. It begins with component suppliers, providing raw materials, spare parts, and advanced technologies such as sensors and electronic systems. Manufacturers and OEMs integrate these components into vehicles and offer long-term support through maintenance contracts. Service providers perform maintenance, repair, and overhaul (MRO) activities, employing predictive and condition-based maintenance to minimize downtime. Technology providers contribute advanced solutions like IoT, AI, and data analytics for monitoring and optimizing vehicle performance. Logistics and supply chain management ensure timely delivery of parts and services to military bases. Governments and defense agencies drive demand through procurement policies, partnerships, and modernization programs, forming the backbone of this dynamic and evolving market.

Military Vehicle Sustainment Market Opportunity Analysis

The military vehicle sustainment market offers significant opportunities driven by advancements in technology, aging fleets, and increased defense spending. Modernization initiatives provide opportunities for upgrading existing vehicles with advanced systems, including IoT-based monitoring, AI-driven diagnostics, and improved weapon integration. The growing emphasis on sustainability and cost efficiency encourages the adoption of predictive maintenance and condition-based systems, reducing operational costs and extending vehicle lifespans. Regional defense initiatives, particularly in Asia-Pacific and the Middle East, create demand for localized sustainment services. Collaboration between governments, OEMs, and private contractors enables the development of innovative solutions, including retrofitting vehicles for multi-mission capabilities. Additionally, global geopolitical tensions drive investment in advanced sustainment technologies, making it a lucrative area for suppliers, technology providers, and service companies to expand their portfolios.

Global Military Vehicle Sustainment Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 18.8 Billion |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | 3.10% |

| 2033 Value Projection: | USD 25.5 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 210 |

| Tables, Charts & Figures: | 111 |

| Segments covered: | Vehicle Type Analysis, End User Analysis, Regional Analysisxxxxxxxxxxxxx |

| Companies covered:: | IDV, Edge Group PJSC, L3Harris Technologies Inc., Amentum, Lockheed Martin Corporation, Elbit Systems Limited, Terma A/S, RTX Corporation, General Dynamics, GS Engineering Inc., Babcock, Thales Group, Larsen & Toubro Limited, CAMMS Shelters, Leonardo DRS Inc., Honeywell International Inc., Indra Sistemas SA, Serco Group Plc, Textron Systems Corporation, BAE Systems Plc, ManTech International Corporation. |

| Pitfalls & Challenges: | COVID-19 Impact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Market Dynamics

Military Vehicle Sustainment Market Dynamics

- Rising implementation of data-driven and predictive maintenance strategies

The growing implementation of data-driven and predictive maintenance strategies is transforming the military vehicle sustainment market. These advanced approaches leverage technologies like IoT, AI, and machine learning to monitor vehicle performance in real time, enabling proactive identification of potential issues before they escalate. This reduces unplanned downtime, enhances operational efficiency, and extends the lifespan of vehicles, making maintenance more cost-effective. Predictive maintenance also supports readiness by ensuring vehicles are mission-ready at all times, a critical factor for defense operations. As defense budgets focus on optimizing resources, demand for these solutions continues to rise. Partnerships between governments, OEMs, and technology providers further accelerate the adoption of predictive systems, driving market growth and shaping the future of vehicle sustainment in the global defense sector.

Restraints & Challenges

Aging fleets require extensive maintenance, leading to high costs and resource demands. The complexity of modern military vehicles, equipped with advanced technologies, necessitates specialized expertise and tools, which can strain budgets and skilled labor availability. Supply chain disruptions, exacerbated by geopolitical tensions and global events, hinder the timely delivery of spare parts and components. Additionally, the integration of data-driven and predictive maintenance systems involves significant initial investments and requires robust cybersecurity measures to protect sensitive data. Variations in defense budgets across regions further complicate long-term planning for sustainment activities. Balancing cost-efficiency with operational readiness remains a persistent challenge, necessitating innovative solutions and collaborative approaches within the industry.

Regional Forecasts

North America Market Statistics

Get more details on this report -

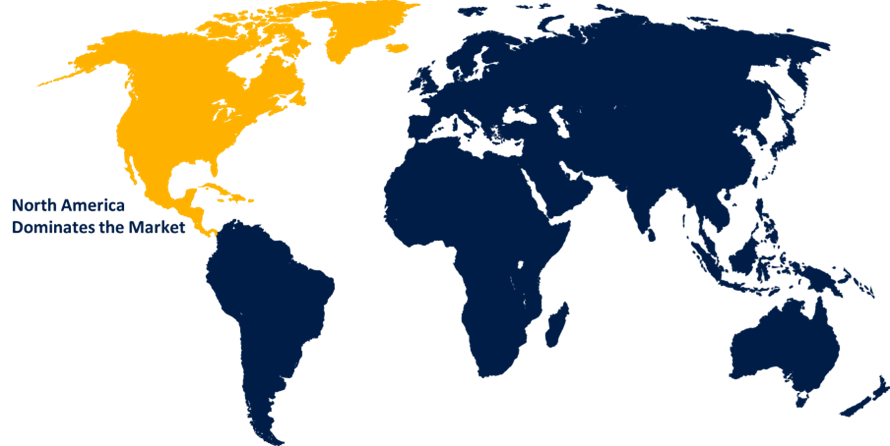

North America is anticipated to dominate the Military Vehicle Sustainment Market from 2023 to 2033. The United States, with the largest defense budget globally, leads in sustainment activities for its extensive fleet of land, air, and naval vehicles. Modernization programs, such as retrofitting vehicles with advanced technologies like AI-driven diagnostics and condition-based maintenance systems, are critical drivers. Canada's defense initiatives also contribute to the market, focusing on maintaining operational readiness and upgrading aging fleets. The presence of major OEMs, advanced technological capabilities, and government-industry partnerships further strengthen the market. Additionally, geopolitical tensions and commitments to allied operations underscore the importance of efficient sustainment practices, fostering continuous innovation and growth in the North American defense sector.

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. China, India, Japan, and South Korea are investing heavily in modernizing their military fleets and enhancing sustainment capabilities to ensure operational readiness. The region's aging vehicle fleets, coupled with a shift toward advanced technologies like predictive maintenance and IoT-based monitoring systems, drive demand for efficient maintenance solutions. Local manufacturing capabilities and partnerships with global OEMs and technology providers are bolstering the market. Additionally, the rise in joint military exercises and strategic alliances emphasizes the need for reliable vehicle performance. As defense priorities evolve, Asia-Pacific remains a key market for innovative sustainment practices and long-term modernization programs.

Segmentation Analysis

Insights by Vehicle Type

The Armored Personnel Carrier segment accounted for the largest market share over the forecast period 2023 to 2033. The growth is driven by rising demand for enhanced troop mobility, protection, and mission versatility. Modernization initiatives, such as retrofitting APCs with advanced armor, communication systems, and weaponry, are fueling sustainment activities. Additionally, the integration of predictive maintenance technologies, like IoT sensors and AI diagnostics, ensures operational readiness and reduces lifecycle costs. The increasing use of APCs in peacekeeping missions and asymmetric warfare underscores the need for sustained performance and reliability. Aging fleets in several regions are also being upgraded to meet modern battlefield requirements. Partnerships between OEMs, defense agencies, and service providers further drive innovation, positioning APCs as a critical segment in the evolving sustainment market landscape.

Insights by End User

The army segment accounted for the largest market share over the forecast period 2023 to 2033. Increased defense budgets and evolving operational needs are pushing armies to prioritize vehicle readiness and extend the lifespan of existing fleets. The demand for advanced technologies, including predictive maintenance, condition-based monitoring, and AI-driven diagnostics, is growing within army fleets to enhance vehicle performance, reduce downtime, and optimize operational costs. Aging vehicle fleets in many countries further contribute to the need for sustainment solutions. Additionally, the army's strategic importance in national defense and peacekeeping missions emphasizes the necessity of reliable, efficient, and cost-effective vehicle sustainment practices, fostering innovation and long-term market growth in this segment.

Recent Market Developments

- In June 2023, Rheinmetall AG introduced an innovative solution for the mobile production of spare parts for military vehicles. The Mobile Smart Factory (MSF) features metal 3D printing and postprocessing capabilities and is seamlessly integrated into Rheinmetall’s IRIS (Integrated Rheinmetall Information System) digital ecosystem.

Competitive Landscape

Major players in the market

- IDV

- Edge Group PJSC

- L3Harris Technologies Inc.

- Amentum

- Lockheed Martin Corporation

- Elbit Systems Limited

- Terma A/S

- RTX Corporation

- General Dynamics

- GS Engineering Inc.

- Babcock

- Thales Group

- Larsen & Toubro Limited

- CAMMS Shelters

- Leonardo DRS Inc.

- Honeywell International Inc.

- Indra Sistemas SA

- Serco Group Plc

- Textron Systems Corporation

- BAE Systems Plc

- ManTech International Corporation

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Military Vehicle Sustainment Market, Vehicle Type Analysis

- Armored Vehicles

- Military Trucks

Military Vehicle Sustainment Market, End User Analysis

- Army

- Navy

- Air Force

Military Vehicle Sustainment Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the market size of the Military Vehicle Sustainment Market?The global Military Vehicle Sustainment Market is expected to grow from USD 18.8 billion in 2023 to USD 25.5 billion by 2033, at a CAGR of 3.10% during the forecast period 2023-2033.

-

2. Who are the key market players of the Military Vehicle Sustainment Market?Some of the key market players of the market are IDV, Edge Group PJSC, L3Harris Technologies Inc., Amentum, Lockheed Martin Corporation, Elbit Systems Limited, Terma A/S, RTX Corporation, General Dynamics, GS Engineering Inc., Babcock, Thales Group, Larsen & Toubro Limited, CAMMS Shelters, Leonardo DRS Inc., Honeywell International Inc., Indra Sistemas SA, Serco Group Plc, Textron Systems Corporation, BAE Systems Plc, ManTech International Corporation.

-

3. Which segment holds the largest market share?The army segment holds the largest market share and is going to continue its dominance.

-

4. Which region dominates the Military Vehicle Sustainment Market?North America dominates the Military Vehicle Sustainment Market and has the highest market share.

Need help to buy this report?