Global Oxy Fuel Combustion Technology Market Size, Share, and COVID-19 Impact Analysis, By Offering (Solution, and Service), By End-user (Oil and Gas, Power Generation, Glass Manufacturing, Industrial, and Metals and Mining), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033

Industry: Energy & PowerGlobal Oxy Fuel Combustion Technology Market Insights Forecasts to 2033

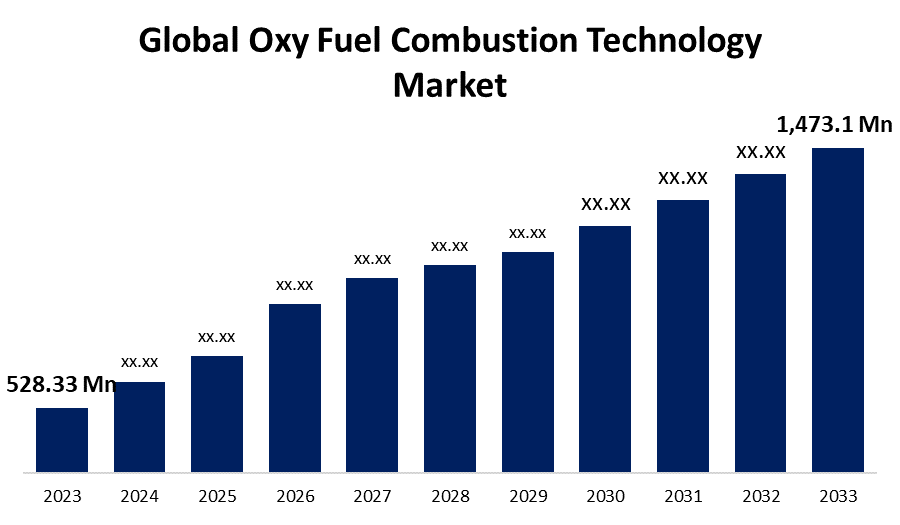

- The Global Oxy Fuel Combustion Technology Market Size was Valued at USD 528.33 Million in 2023

- The Market Size is Growing at a CAGR of 10.8% from 2023 to 2033

- The Worldwide Oxy Fuel Combustion Technology Market Size is Expected to Reach USD 1,473.1 Million by 2033

- Asia Pacific is Expected to Grow the fastest during the forecast period.

Get more details on this report -

The Global Oxy Fuel Combustion Technology Market Size is Anticipated to Exceed USD 1,473.1 Million by 2033, Growing at a CAGR of 10.8% from 2023 to 2033.

Market Overview

In oxy-fuel combustion technology, coal, oil, or natural gas combusts in pure oxygen rather than in normal air. Precisely, normally, the air contains approximately 21% oxygen and 78% nitrogen, but this technology separates nitrogen away, leaving only pure oxygen. This is bound to produce several advantages; in that it improves combustion to higher temperatures and more complete fuel burn. While this is the case, it cuts down nitrogen oxide which is a dangerous pollutant. Carbon dioxide capturing from the waste gases is much easier in oxy-fuel combustion, and that is one of the major advantages of the process. After the nitrogen is taken out, flue gas will be mainly Carbon dioxide and water vapor. In such a scenario, it's less complicated to isolate and store Carbon dioxide for prevention from atmospheric release. This is very beneficial in terms of greenhouse gas emissions reduction and, thus, helps in the fight against climate change. Several industries, such as power generation and metal production, are studying and adopting oxy-fuel combustion because it offers a cleaner and much more efficient option for managing energy use with limited environmental degradation.

Report Coverage

This research report categorizes the market for the global oxy fuel combustion technology market based on various segments and regions forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global oxy fuel combustion technology market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global oxy fuel combustion technology market.

Global Oxy Fuel Combustion Technology Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 528.33 Million |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | 10.8% |

| 2033 Value Projection: | USD 1,473.1 Million |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 220 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Offering, By End-use, By Region |

| Companies covered:: | Falorni Gianfrance SRL, General Electric Co, HeidelbergCement AG, Hitachi Ltd, Jupiter Oxygen Corp, Linde Plc, Air Liquide SA, Air Products & Chemicals Inc, Encon Thermal Engineers Pvt Ltd, ESA SpA, Praxair Technology Inc, Mitsubishi Hitachi Power Systems, Ltd., NGK SPARK PLUG CO., LTD., GE Vernova, IHI, and other key companies. |

| Pitfalls & Challenges: | Covid-19 Empact, Challenges, Growth, Analysis. |

Get more details on this report -

Driving Factors

Strict Environmental Regulations

Several countries have imposed stringent limits on the number of emissions from power plants because of increasing concerns over air pollution and climate change. While NOx emissions can be reduced, the oxyfuel combustion technology can help power plants meet such regulations and give higher carbon capture efficiency. The large Combustion Plant Directive by the European Union prescribes emission limits for a range of pollutants from large combustion plants. Additionally, there is encouragement towards the adoption of technologies like oxyfuel combustion. A number of regions have enacted renewable energy portfolio standards too, which require a percentage of electricity generation from renewable sources. Oxyfuel combustion can be combined with various renewable energy technologies to offer further sustainability in power generation. In fact, with the increasing emphasis around the world on environmental sustainability, this market trend of oxyfuel combustion technology is standing prepared to help lead to a low-carbon future.

Restraining Factors

High Cost of Oxy Fuel Combustion Technology

Oxyfuel combustion is expensive and energy-intensive, which raises the price of electricity generated by oxyfuel plants. Also, retrofitting existing industrial facilities to accommodate oxyfuel combustion can be expensive.

Market Segmentation

The global oxy fuel combustion technology market share is classified into offering and end-user.

- The solution segment is expected to hold the largest share of the global oxy fuel combustion technology market during the forecast period.

Based on the offering, the global oxy fuel combustion technology market is categorized into solution, and service. Among these, the solution segment is expected to hold the largest share of the global oxy fuel combustion technology market during the forecast period. Solutions include a variety of components and technologies that allow for efficient combustion in oxygen-rich environments, improve carbon capture, and integrate with existing industrial infrastructure. This includes oxygen separation units, combustion systems, carbon capture and storage (CCS) technology, and control and monitoring systems. Oxyfuel combustion solutions aim to address high-temperature combustion, emissions reduction, and the extraction of concentrated CO2 for storage or use. These integrated solutions contribute to the broader goals of environmental sustainability and the transition to low-carbon industrial processes.

- The glass manufacturing segment is expected to grow at the fastest CAGR during the forecast period.

Based on the end-user, the global oxy fuel combustion technology market is categorized into oil and gas, power generation, glass manufacturing, industrial, and metals and mining. Among these, the glass manufacturing segment is expected to grow at the fastest CAGR during the forecast period. Glass is a recyclable and sustainable material manufactured for industrial products, from dinnerware and flat glass to LCDs, computers, and even windows intended for various automotive and construction industries. Most glass manufacturing processes include glass melting furnaces in which Oxy-fuel combustion technology is used. Oxy-fuel technology in combustion a technology that uses oxygen-enriched air can give higher temperatures and more efficient heating. The IEA estimates that the glass manufacturing industry emits more than 60 megatons of carbon dioxide. An expanding population and rapid growth in the infrastructure sector drives demand for glass.

Regional Segment Analysis of the Global Oxy Fuel Combustion Technology Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is projected to hold the largest share of the global oxy fuel combustion technology market over the forecast period.

Get more details on this report -

North America is projected to hold the largest share of the global oxy fuel combustion technology market over the forecast period. Oxyfuel combustion technology is overwhelmingly backed by North America, an area that has a strict government that ensures environmental air quality. The region has adopted new energy policies like cap-and-trade policies that have been implemented by some companies and countries, while at the same time promoting the reduction of GHGe. Following procedures such as selecting the optimal technology for the different pollution sources, the government would phase out those harmful greenhouse gases. These and other intended measures will reach a Green GDP of 10 to 20 percent.

Asia Pacific is expected to grow at the fastest CAGR growth of the global oxy fuel combustion technology market during the forecast period. Asia-Pacific offers significant growth opportunities for participants in the oxyfuel combustion technology market due to the region's increasing urbanization and industrialization. Rising population and living standards have increased the region's energy demand, prompting more investment in power plants. Given the favorable government regulations and availability of resources, several industries have relocated their manufacturing facilities to the region, increasing CO2 emissions. To meet rising customer demand, corporations have expanded production facilities into new markets such as China and India.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global oxy fuel combustion technology market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Falorni Gianfrance SRL

- General Electric Co

- HeidelbergCement AG

- Hitachi Ltd

- Jupiter Oxygen Corp

- Linde Plc

- Air Liquide SA

- Air Products & Chemicals Inc

- Encon Thermal Engineers Pvt Ltd

- ESA SpA

- Praxair Technology Inc

- Mitsubishi Hitachi Power Systems, Ltd.

- NGK SPARK PLUG CO., LTD.

- GE Vernova

- IHI

- Others

Key Market Developments

- In January 2024, Hitachi announced the completion of an absorption-type split agreement to strengthen its energy and facility management services business through a company split.

- In January 2024, GE Vernova and IHI announced the next step in their technology roadmap, which aims to develop a gas turbine combustion system capable of using 100% ammonia by 2030.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. Spherical Insights has segmented the global oxy fuel combustion technology market based on the below-mentioned segments:

Global Oxy Fuel Combustion Technology Market, By Offering

- Solution

- Service

Global Oxy Fuel Combustion Technology Market, By End-user

- Oil and Gas

- Power Generation

- Glass Manufacturing

- Industrial

- Metals and Mining

Global Oxy Fuel Combustion Technology Market, By Regional

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Need help to buy this report?