Global Semiconductor Foundry Market Size, Share, and COVID-19 Impact Analysis, By Technology Node (10/7/5nm, 16/14nm, 20nm, 28 nm, 45/40nm, and Others), By Foundry Type (Pure Play Foundry, IDMs), By Application (Communication, Consumer Electronics, Computer, Automotive, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033

Industry: Semiconductors & ElectronicsGlobal Semiconductor Foundry Market Insights Forecasts to 2033

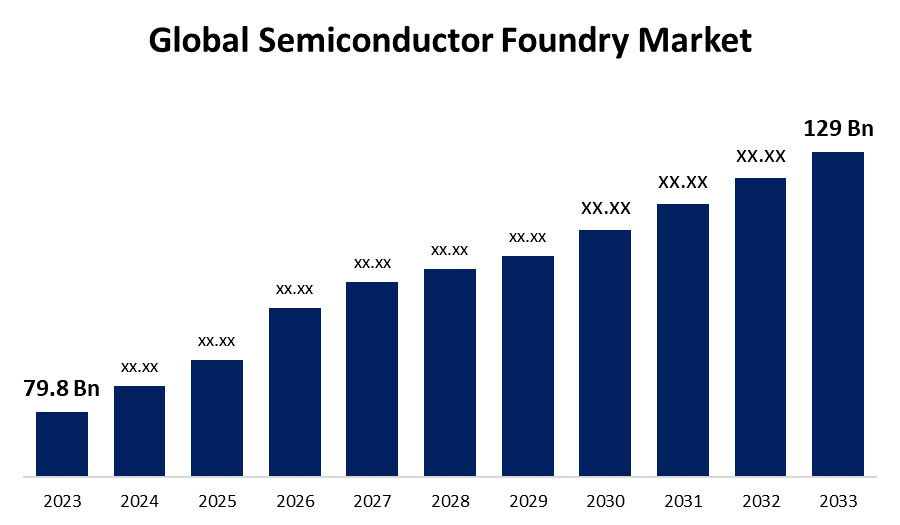

- The Global Semiconductor Foundry Market Size was Valued at USD 79.8 Billion in 2023

- The Market Size is Growing at a CAGR of 4.92% from 2023 to 2033

- The Worldwide Semiconductor Foundry Market Size is Expected to Reach USD 129 Billion by 2033

- North America is Expected to Grow the fastest during the forecast period.

Get more details on this report -

The Global Semiconductor Foundry Market Size is Anticipated to Exceed USD 129 Billion by 2033, Growing at a CAGR of 4.92% from 2023 to 2033.

Market Overview

A semiconductor foundry, also known as a fab or fabrication plant, is a factory that manufactures integrated circuits (ICs) using silicon wafers for other companies on a large scale. These ICs are the fundamental components that power several electronic devices. Semiconductor foundries are crucial for the production of chips designed by semiconductor companies, especially those that focus only on design and outsource the manufacturing process.

The manufacturing process in a semiconductor foundry involves multiple stages which include photolithography, etching, doping, and the deposition of various materials to create the intricate layers that make up modern chips. There are different types of semiconductor foundries. Pure-play foundries and integrated device manufacturers (IDMs) are the most common. Pure-play foundries, such as TSMC (Taiwan Semiconductor Manufacturing Company), focus solely on manufacturing semiconductor products for other companies and do not design their chips. IDMs like Intel and Samsung design and manufacture their chips, and also produce them for other companies. Companies that design chips but do not have manufacturing capabilities, known as fabless companies such as AMD, Qualcomm, and NVIDIA rely on foundries for manufacturing.

Semiconductors and electronics are the foundation of modern technology. It is used in smartphones, cloud servers, modern cars, industrial automation, critical infrastructure, and defense systems. Semiconductor foundries play an essential role in the electronics industry.

Report Coverage

This research report categorizes the market for the global semiconductor foundry market based on various segments and regions forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global semiconductor foundry market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global semiconductor foundry market.

Global Semiconductor Foundry Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023 : | USD 79.8 Billion |

| Forecast Period: | 2023 – 2033 |

| Forecast Period CAGR 2023 – 2033 : | 4.92% |

| 023 – 2033 Value Projection: | USD 129 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 247 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Technology Node, By Foundry Type, By Application, By Region |

| Companies covered:: | Samsung Group, STMicroelectronics NV, DB HiTek, United Microelectronics Corporation (UMC), Fujitsu Semiconductor Limited, TowerJazz (Tower Semiconductor Limited), Magnachip, Nexchip, GlobalFoundries, Powerchip Semiconductor Manufacturing Corp., HH Grace, Taiwan Semiconductor Manufacturing Company (TSMC) Limited, X-FAB Silicon Foundries, Vanguard International Semiconductor Corporation, Semiconductor Manufacturing International Corporation (SMIC), Others |

| Pitfalls & Challenges: | Covid-19 Impact, Challenge, Future,Growth and Analysis |

Get more details on this report -

Driving Factors

The growing demand for consumer electronics, such as smartphones, tablets, and wearables, is a primary catalyst, necessitating high-performance and energy-efficient semiconductor solutions. Additionally, rapid advancements in artificial intelligence (AI), machine learning (ML), deep learning (DL), cryptography, and blockchain are fueling the need for advanced chips capable of handling complex mathematical calculations and large data sets.

The rise of the Internet of Things (IoT) devices and GPUs are other driving factors, as these devices need high-speed semiconductors to function seamlessly. In the automotive sector, the shift towards electric and self-driving vehicles fuels the demand for semiconductor components, given their critical role in vehicle control and smart functionalities. Furthermore, the technology is fuelling the need for new semiconductor designs to support faster and more reliable communication networks.

Restraining Factors

High capital expenditure is a major barrier, as establishing and maintaining cutting-edge manufacturing factories need huge financial resources. Additionally, supply chain disruptions caused by geopolitical tensions and natural disasters can significantly impact production and delivery schedules, leading to potential market volatility. Intense competition in the industry forces companies to operate on low-profit margins, which might limit their ability to invest in long-term innovations. The rapid technological changes necessitate continuous upgrades, which could disturb the production line of semiconductor foundries.

Market Segmentation

The global semiconductor foundry market share is classified into technology node, foundry type, and application.

- The 10/7/5nm segment is expected to hold the largest share of the global semiconductor foundry market during the forecast period.

Based on the technology node, the global semiconductor foundry market is divided into 10/7/5nm, 16/14nm, 20nm, 28 nm, 45/40nm, and others. Among these, the 10/7/5nm segment is expected to hold the largest share of the global semiconductor foundry market during the forecast period. The 10/7/5nm nodes offer higher transistor density, allowing manufacturers to pack more functionality into small chips, which boosts performance. It is crucial for high-demand applications in consumer electronics, like smartphones and high-performance computing and gaming devices, where power efficiency and performance are needed. They deliver better energy efficiency, faster processing speeds, and improved performance, making them an attractive option for technology firms.

- The IDMs segment is expected to hold the largest share of the global semiconductor foundry market during the forecast period.

Based on foundry type, the global semiconductor foundry market is divided into pure-play foundries and IDMs. Among these, the IDMs segment is expected to hold the largest share of the global semiconductor foundry market during the forecast period. IDMs stand for integrated device manufacturers. IDMs, such as Intel and Samsung, dominate the market as they control the entire production process from design to manufacturing. This vertical integration allows them to optimize efficiencies, reduce costs, and ensure superior quality control across the production lifecycle. IDMs benefit from significant economies of scale and substantial capital resources, enabling them to invest heavily in newer technologies and advanced manufacturing capabilities. Furthermore, IDMs often have established, long-term relationships with customers, this ensures constant demand and stable revenue streams.

- The communication segment is expected to grow at the fastest CAGR in the global semiconductor foundry market during the forecast period.

Based on application, the global semiconductor foundry market is divided into communication, consumer electronics, computer, automotive, and others. Among these, the communication segment is expected to grow at the fastest CAGR in the global semiconductor foundry market during the forecast period. This rapid growth is driven by the roll-out and adoption of 5G technology worldwide. The demand for cutting-edge chips in this segment is skyrocketing as 5G networks require semiconductors to handle higher data speeds, lower latency, and improve connectivity. Moreover, the spread of smartphones, tablets, and other communication devices necessitates constant innovation and integration of advanced semiconductor solutions. Additionally, the growing trend of smart homes and IoT-enabled devices, which rely on seamless communication and connectivity, fuels this rapid expansion.

Regional Segment Analysis of the Global Semiconductor Foundry Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia-Pacific is anticipated to hold the largest share of the global semiconductor foundry market over the predicted timeframe.

Get more details on this report -

Asia-Pacific is anticipated to hold the largest share of the global semiconductor foundry market over the predicted timeframe. The regional market is driven by major industry players such as TSMC (Taiwan Semiconductor Manufacturing Company) and Samsung, who lead the market in advanced semiconductor manufacturing. The region benefits from a robust and well-established electronics manufacturing infrastructure, supported by significant investments in technology and innovation.

Moreover, Asia-Pacific countries, particularly Taiwan, South Korea, and China have emerged as global manufacturing hubs due to their skilled workforce, favorable government policies, and extensive research and development capabilities. The high demand for consumer electronics and automotive components further drives the semiconductor foundry market in this region. Additionally, the rapid growth of emerging technologies, such as 5G and IoT, in Asia-Pacific contributes to the sustained high demand for advanced semiconductor solutions, reinforcing its position as the largest market share holder in this industry.

North America is expected to grow at the fastest pace in the global semiconductor foundry market during the forecast period. This growth is driven by innovations in AI, machine learning, and autonomous vehicles. Additionally, North America has several leading tech companies and fabless semiconductor firms, like Apple and NVIDIA, which rely heavily on foundry services for their high-performance chip designs. The rising investments in semiconductor manufacturing capabilities, combined with government initiatives to boost domestic production and reduce supply chain dependencies, fuel this growth. Moreover, the rapid adoption of 5G technology and the expanding IoT ecosystem creates demand for advanced semiconductor solutions, positioning the region for the fastest growth in this market.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global semiconductor foundry market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Samsung Group

- STMicroelectronics NV

- DB HiTek

- United Microelectronics Corporation (UMC)

- Fujitsu Semiconductor Limited

- TowerJazz (Tower Semiconductor Limited)

- Magnachip

- Nexchip

- GlobalFoundries

- Powerchip Semiconductor Manufacturing Corp.

- HH Grace

- Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- X-FAB Silicon Foundries

- Vanguard International Semiconductor Corporation

- Semiconductor Manufacturing International Corporation (SMIC)

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In September 2024, South Korea’s Samsung Electronics Co., the world’s largest memory chipmaker, partnered with its foundry rival Taiwan Semiconductor Manufacturing Co. (TSMC) to jointly develop a next-generation artificial intelligence chip, HBM4, in a push to strengthen their positions in the fast-growing AI chip market.

- In March 2024, Tata Group aims to begin commercial production from India’s first semiconductor fabrication unit by 2026, an aggressive timeline considering the country’s long wait to become self-reliant in chips that power technology ranging from smartphones to defense systems.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. Spherical Insights has segmented the global semiconductor foundry market based on the below-mentioned segments:

Global Semiconductor Foundry Market, By Technology Node

- 10/7/5nm

- 16/14nm

- 20nm

- 28nm

- 45/40nm

- Others

Global Semiconductor Foundry Market, By Foundry Type

- Pure Play Foundry

- IDMs

Global Semiconductor Foundry Market, By Application

- Communication

- Consumer Electronics

- Computer

- Automotive

- Others

Global Semiconductor Foundry Market, Regional

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Need help to buy this report?