United States Practice Management Systems Market Size, Share, and COVID-19 Impact Analysis, By Product (Integrated and Standalone), By Component (Software and Services), By Delivery Mode (On Premise, Web-Based, and Cloud-Based), By End-use (Physician Back Office, Pharmacies, Diagnostic Laboratories, and Other Settings), and United States Practice Management Systems Market Insights, Industry Trend, Forecasts to 2033

Industry: HealthcareUnited States Practice Management Systems Market Insights Forecasts to 2033

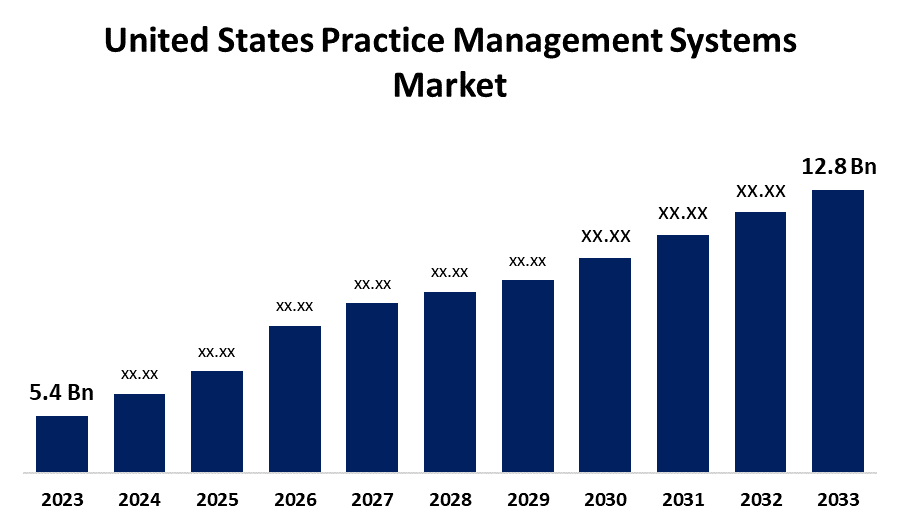

- The United States Practice Management Systems Market Size was valued at USD 5.4 billion in 2023.

- The Market is growing at a CAGR of 9.01% from 2023 to 2033

- The U.S. Practice Management Systems Market Size is expected to reach USD 12.8 billion by 2033

Get more details on this report -

The United States Practice Management Systems Market is anticipated to exceed USD 12.8 billion by 2033, growing at a CAGR of 9.01% from 2023 to 2033. The growing focus on the implementation of high-quality care and cost-effectiveness, strategic initiatives by the key players to provide cloud-based solutions, and the development of new value-added services are driving the growth of the practice management systems market in the United States.

Market Overview

Practice management systems are systems that handle the day-to-day management of medical practice. Using medical practice management software facilitates operational efficiency, and accurate claims generation in/with faster reimbursements. Practice management software providers and organizations have started to use practice management software to schedule patient appointments, improve data availability through EHRs, and mainstream telehealth as ways to combat the epidemic. The government budget for research and development in the United States increased from USD 3.5 billion in 1955 to USD 137.8 billion in 2020, according to a report by the Congressional Research Service. Thus, the rising R&D activities are anticipated to propel the market growth for practice management systems in the US. The use of practice management systems is primarily driven by the rising need to achieve operational efficiency, improved documentation with minimal errors, and financial viability for physician practices. Furthermore, the quick adoption of IT and the growing number of encouraging federal initiatives in the US that integrate health records on a single platform are expected to leverage market opportunities.

Report Coverage

This research report categorizes the market for the US practice management systems market based on various segments and regions and forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the practice management systems market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the practice management systems market.

United States Practice Management Systems Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 5.4 billion |

| Forecast Period: | 2023 to 2033 |

| Forecast Period CAGR 2023 to 2033 : | 9.01% |

| 2033 Value Projection: | USD 12.8 billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 250 |

| Tables, Charts & Figures: | 115 |

| Segments covered: | By Product, By Component, By Delivery Mode, By End-use and COVID-19 Impact Analysis |

| Companies covered:: | Henry Schein, Inc., Veradigm LLC (Allscripts Healthcare, LLC), GE Healthcare, McKesson Corporation, Athenahealth, Inc., eClinicalWorks, CareCloud, Inc., AdvantEdge Healthcare Solutions, EPIC Systems Corporation, NXGN Management, LLC., Cerner Corporation (Oracle), Kareo, Inc., AdvancedMD, Inc., CollaborateMD Inc. (EverCommerce), DrChrono, Inc. (EverCommerce), OfficeAlly Inc., and others Key players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The growing need to reduce healthcare costs as well as the changing dynamics of hospital/healthcare settings are driving the market. The increasing emphasis on the implementation of high-quality care and cost-effectiveness also contributes to market growth. Further, the strategic initiatives taken by the key players to offer cloud-based solutions to their clients are driving the US practice management systems market. The incorporation of practice management systems with other healthcare IT solutions, like laboratory information systems and computerized physician order entry (CPOE) is anticipated to drive the market growth.

Restraining Factors

The increasing concerns about patient information security and privacy are restraining the US practice management systems market. The risk of information leaks and potential data misuse or manipulation associated with the use of cloud-based MPMS may hamper the market growth.

Market Segmentation

The United States Practice Management Systems Market share is classified into product, component, delivery mode, and end-use.

- The integrated segment dominates the market with the largest market share in 2023.

The United States practice management systems market is segmented by product into integrated and standalone. Among these, the integrated segment dominates the market with the largest market share in 2023. Integrated segment is further segmented into billing systems, e-Rx, electronic health records (EHR), and patient interaction. The increasing popularity of integrated systems due to the trend towards centralization in healthcare has led to drive the market.

- The software segment accounted for the largest share of the United States practice management systems market in 2023.

Based on the component, the United States Practice Management Systems market is divided into software and services. Among these, the software segment accounted for the largest share of the United States practice management systems market in 2023. The increasing technological advancements and government reforms in the healthcare IT sector have driven the market growth in the software segment.

- The web-based segment accounted for the largest share of the United States practice management systems market in 2023.

Based on the delivery mode, the United States practice management systems market is divided into on premise, web-based, and cloud-based. Among these, the web-based segment accounted for the largest share of the

United States practice management systems market in 2023. The advantageous features of web-based practice management systems such as affordability, quick Return on Investment (RoI), and ease of deployment are driving the practice management systems market.

- The physician back office segment dominated the market with the largest market share during the forecast period.

The United States practice management systems market is segmented by end-use into physician back office, pharmacies, diagnostic laboratories, and other settings. Among these, the physician back office segment dominated the market with the largest market share during the forecast period. The growing demand for effective revenue cycle management and improvement of efficiency and operations in medical practices through the adoption of a clear organizational structure are driving the market expansion.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the US practice management systems market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Henry Schein, Inc.

- Veradigm LLC (Allscripts Healthcare, LLC)

- GE Healthcare

- McKesson Corporation

- Athenahealth, Inc.

- eClinicalWorks

- CareCloud, Inc.

- AdvantEdge Healthcare Solutions

- EPIC Systems Corporation

- NXGN Management, LLC.

- Cerner Corporation (Oracle)

- Kareo, Inc.

- AdvancedMD, Inc.

- CollaborateMD Inc. (EverCommerce)

- DrChrono, Inc. (EverCommerce)

- OfficeAlly Inc.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In January 2024, CareCloud, Inc., a leader in health care technology solutions for medical practices and health systems nationwide, announced a strategic collaboration with Kovo HealthTech Corporation, a leader in healthcare technology and Billing-as-a-Service. This landmark partnership is designed to empower Kovo clients with an advanced suite of electronic health record (EHR) solutions, cutting-edge practice management software, unparalleled credentialing support, and an integrated clearinghouse.

- In December 2023, Veradigm Inc., a leading provider of healthcare data and technology solutions, to offer a conversational artificial intelligence (AI) agent for Practice Fusion Billing Services, a Veradigm Network solution. This enhancement would help simplify the billing process and optimize financial management for independent healthcare providers.

Market Segment

This study forecasts revenue at United States, regional, and country levels from 2020 to 2033. Spherical Insights has segmented the United States Practice Management Systems Market based on the below-mentioned segments:

United States Practice Management Systems Market, By Product

- Integrated

- Standalone

United States Practice Management Systems Market, By Component

- Software

- Services

United States Practice Management Systems Market, By Delivery Mode

- On Premise

- Web-Based

- Cloud-Based

United States Practice Management Systems Market, By End-use

- Physician Back Office

- Pharmacies

- Diagnostic Laboratories

- Other Settings

Need help to buy this report?