Global Viral Vector And Plasmid DNA Manufacturing Market Size, Share, and COVID-19 Impact Analysis, By Application (Antisense & RNAi Therapy, Gene Therapy, Cell Therapy, Vaccinology, and Research Applications), By Disease (Cancer, Genetic Disorders, Infectious Diseases, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033.

Industry: HealthcareGlobal Viral Vector And Plasmid DNA Manufacturing Market Insights Forecasts to 2033

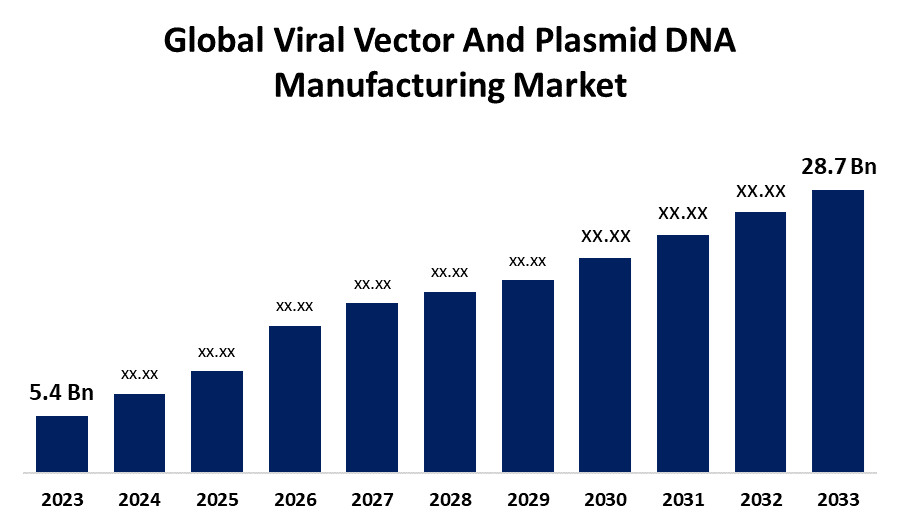

- The Global Viral Vector And Plasmid DNA Manufacturing Market Size was Valued at USD 5.4 Billion in 2023

- The Market Size is Growing at a CAGR of 18.18% from 2023 to 2033

- The Worldwide Viral Vector And Plasmid DNA Manufacturing Market Size is Expected to Reach USD 28.7 Billion by 2033

- Asia Pacific is Expected to Grow the fastest during the forecast period.

Get more details on this report -

The Global Viral Vector And Plasmid DNA Manufacturing Market Size is Anticipated to Exceed USD 28.7 Billion by 2033, Growing at a CAGR of 18.18% from 2023 to 2033.

Market Overview

In the field of molecular, genetics a vector is any particle with the ability to carry foreign DNA into a cell, where the DNA will be replicated or something that will be expressed. A viral vector is a virus used as a vector, that is genetically modified and a plasmid is a type of vector that is a small circular DNA. A viral vector is a virus that has hence been modified with the intention of using it to transfer material with a specific sequence into a cell. Engineering specimens of Viral vectors are used in gene therapy, agriculture as well as in explorations of research. They are made by changing a virus in a laboratory so that it cannot lead to any disease which is called a plasmid, circular spherical structure, which can be observed in bacteria and also in other life forms. Plasmids are not part of the chromosomal DNA have an independent existence and also have their own mode of replication. Many of these vectors are plasmids, and they can be kept in the host cells by a transformation procedure.

According to the United States Food and Drug Administration, DNA vaccines are viewed as purified plasmid preparations, which contain one or several DNA sequences capable of producing and/or stimulating an immune response to a pathogen. Normally, such plasmids contain genes that are required for their recognition and replication in bacteria. Furthermore, they possess eukaryotic promoters and enhancers and transcription termination/-polyadenylation sequences for gene expression in vaccinated individuals and may be endowed with immunomodulatory components. DNA Anti-body vaccines are organized biologicals in terms of the PHS ACT section 351 which defines them as biological products (42 U. S. C. 262). DNA Anti-body vaccines are managed and controlled by the FDA ‘s Center for Biologics Evaluation and Research (CBER). The main guidelines associated with DNA vaccines are regulated under Title 21 of the Code of Federal Regulations CFR-Parts-210, 211, 312, 600, and 601 and subpart H, part 610. Other documents which are also produced by CBER include information that may be useful for DNA vaccines as follows.

Report Coverage

This research report categorizes the market for viral vector and plasmid DNA manufacturing based on various segments and regions forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the viral vector and plasmid DNA manufacturing market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the viral vector and plasmid DNA manufacturing market.

Global Viral Vector And Plasmid DNA Manufacturing Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 5.4 Billion |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | 18.18% |

| 2033 Value Projection: | USD 28.7 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 250 |

| Tables, Charts & Figures: | 120 |

| Segments covered: | By Application, By Disease, By Region and COVID-19 Impact Analysis |

| Companies covered:: | Merck KGaA, Lonza, FUJIFILM Diosynth Biotechnologies, Thermo Fisher Scientific, Cobra Biologics, Catalent Inc., Wuxi Biologics, Takara Bio Inc., Waisman Biomanufacturing, Genezen laboratories, Batavia Biosciences, Miltenyi Biotec GmbH, SIRION Biotech GmbH, Virovek Incorporation and others Key vendors. |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The market for viral vector and plasmid DNA manufacturing has many influencing factors that have led to the growth of this market. They include high investment in Gene therapy and vaccines most of which require efficient viral vector and plasmid DNA manufacturing. Moreover, there are improvements in demands and effectiveness in treatment by biotechnology as well as genetic engineering. The favorable stance by the regulatory authorities towards gene therapies and a growing number of clinical trials are even further growing the market. The inexorable increase in the occurrence of genetic disorders as well as infectious diseases demands novel and optimum manufacturing approaches. A rise in the number of patients who opt for gene therapy products, therefore increases the market in the long-term. It is evident that as research and development in gene therapy advances there is increased demand for plasmid DNA. Therefore, for AAV, lentivirus, and other viral vector systems, it is mandatory to have pDNA (Plasmid DNA) production.

Restraining Factors

The manufacturing market challenges or barriers exist in the viral vector and plasmid DNA market which shows the potential for growth. Possible implications of the advanced manufacturing technologies on the overall production con include; The high cost of production might act as a barrier to any small enterprises from venturing into the market. Further, the high level of regulatory compliance and sophistication of production systems are barriers to manufacturers. Maintaining Quality control and Quality assurance leads to more time required for the production of any product hence changing the markets.

Market Segmentation

The viral vector and plasmid DNA manufacturing market share is classified into application and disease.

- The vaccinology segment is estimated to hold the highest market revenue share through the projected period.

Based on the application, the viral vector and plasmid DNA manufacturing market is classified into antisense & RNAi therapy, gene therapy, cell therapy, vaccinology, and research applications. Among these, the vaccinology segment is estimated to hold the highest market revenue share through the projected period. This is so because of the increased need for vaccines particularly given the situation where there is an outbreak of diseases around the world. Special development emphasis has been created on viral vectors due to demands for biosecurity vaccines for emerging diseases. The recent breakthroughs in the mRNA vaccines have revived the focus on the viral vectors in order to amplify the immunogenicity. The focus on productive and cost-effective production methodologies will solidify the vaccinology segment as the front-runner among governments and organizations that seek efficient vaccine production capacities. Another factor for this segment’s revenue growth is the exerted constant efforts in the development of new vaccines for new as well as existing infectious diseases, and cancer.

- The cancer segment is anticipated to hold the largest market share through the forecast period.

Based on the disease, the viral vector and plasmid DNA manufacturing market is divided into cancer, genetic disorders, infectious diseases, and others. Among these, the cancer segment is anticipated to hold the largest market share through the forecast period. Market expansions are expected in the Viral Vector and Plasmid DNA manufacturing market, majorly due to the growing cases of cancer all over the world. The use of viral vectors in the formation of exceptional therapies and in line with the concept of personalized medicine is slowly coming into practice and the treatment is highly likely. Non-viral vectors are widely utilized in oncogene therapy, and effective viral vectors for gene transfer are important regarding gene-therapy applications in oncology as well as research efforts and clinical trials that aim to develop an ever-widening range of novel treatment options. With the global concern for cancer solutions increasing, there is expected to be increased investment in enhancements of efficient manufacturing techniques for viral vectors and plasmid DNA hence strengthening this segment of the market.

Regional Segment Analysis of the Viral Vector And Plasmid DNA Manufacturing Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the viral vector and plasmid DNA manufacturing market over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the largest share of the viral vector and plasmid DNA manufacturing market over the predicted timeframe. This is due to robust biotechnology infrastructure and significant investments in research and development. Major pharmaceutical companies and biotech firms are heavily engaged in developing advanced therapies, particularly in gene editing and personalized medicine. The presence of leading academic institutions and research organizations fosters innovation and collaboration in this field, while regulatory support and streamlined approval processes for gene therapies contribute to the region's market leadership. As healthcare expenditures continue to rise, North America is poised to maintain its position at the forefront of viral vector and plasmid DNA manufacturing.

Asia Pacific is expected to grow at the fastest CAGR growth of the viral vector and plasmid DNA manufacturing market during the forecast period. The growth is propelled by increasing investments in the biotechnology and pharmaceutical sectors, alongside a rising prevalence of genetic disorders and infectious diseases. Countries like China and India are expanding their R&D capabilities and manufacturing facilities to attract global players seeking cost-effective solutions. Government initiatives to enhance healthcare infrastructure and foster innovation in life sciences are further propelling market growth. The growing interest in personalized medicine and gene therapies in this region indicates a promising future for viral vector and plasmid DNA manufacturing, making it an attractive area for investment. ). Also, patients from the West are gradually traveling to Asia for stem cell therapy, where regulations are easier to impose. In addition, international corporations have shifted their focus to the region because of its vast population and unmet potential.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the viral vector and plasmid DNA manufacturing market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Merck KGaA

- Lonza

- FUJIFILM Diosynth Biotechnologies

- Thermo Fisher Scientific

- Cobra Biologics

- Catalent Inc.

- Wuxi Biologics

- Takara Bio Inc.

- Waisman Biomanufacturing

- Genezen laboratories

- Batavia Biosciences

- Miltenyi Biotec GmbH

- SIRION Biotech GmbH

- Virovek Incorporation

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In June 2024, Charles River Laboratories International Inc. and Captain T Cell, a spinoff from the Max Delbrück Center Berlin, Germany, signed a plasmid DNA and retrovirus vector production program agreement.

- In June 2024, ProBio Inc., a New Jersey-based contract development and manufacturing organization (CDMO), proudly announce the expansion of its plasmid DNA and viral vector manufacturing capabilities with the opening of a new state-of-the-art facility in Hopewell, New Jersey. This cutting-edge facility will serve as the hub for North American operations, significantly enhancing ProBio's capability to support the manufacturing of life-changing cell and gene therapies in North America.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2023 to 2033. Spherical Insights has segmented the viral vector and plasmid DNA manufacturing market based on the below-mentioned segments:

Global Viral Vector And Plasmid DNA Manufacturing Market, By Application

- Antisense & RNAi Therapy

- Gene Therapy

- Cell Therapy

- Vaccinology

- Research Applications

Global Viral Vector And Plasmid DNA Manufacturing Market, By Disease

- Cancer

- Genetic Disorders

- Infectious Diseases

- Others

Global Viral Vector And Plasmid DNA Manufacturing Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the CAGR of the viral vector and plasmid DNA manufacturing market over the forecast period?The viral vector and plasmid DNA manufacturing market is projected to expand at a CAGR of 18.18% during the forecast period.

-

2. What is the market size of the viral vector and plasmid DNA manufacturing market?The Global Viral Vector And Plasmid DNA Manufacturing Market Size is Expected to Grow from USD 5.4 Billion in 2023 to USD 28.7 Billion by 2033, at a CAGR of 18.18% during the forecast period 2023-2033.

-

3. Which region holds the largest share of the viral vector and plasmid DNA manufacturing market?North America is anticipated to hold the largest share of the viral vector and plasmid DNA manufacturing market over the predicted timeframe.

Need help to buy this report?